-

下載億題庫APP

-

聯(lián)系電話:400-660-1360

下載億題庫APP

聯(lián)系電話:400-660-1360

請謹(jǐn)慎保管和記憶你的密碼,以免泄露和丟失

請謹(jǐn)慎保管和記憶你的密碼,以免泄露和丟失

Portfolio Expected Return and Variance of Return

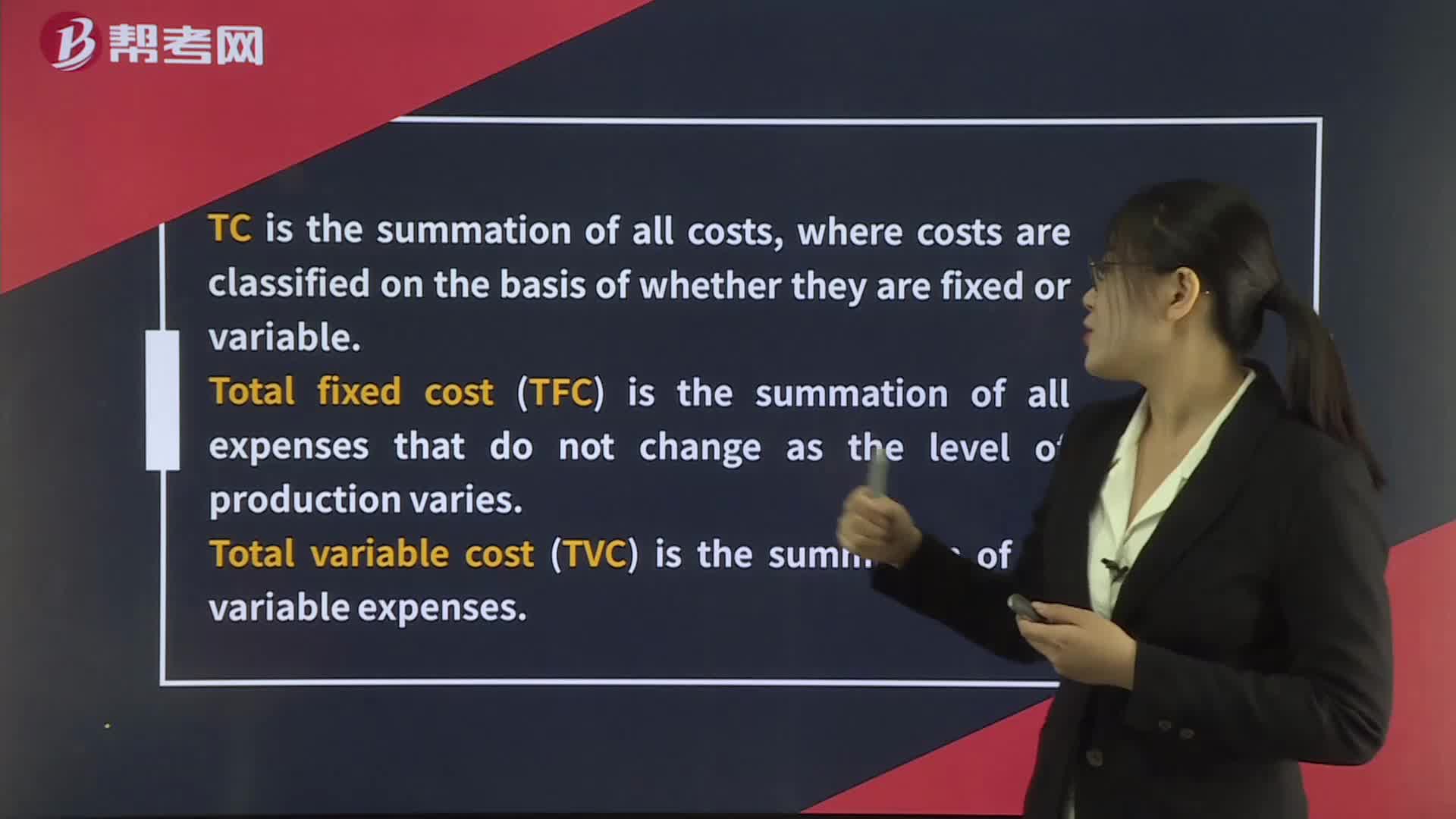

Total, Variable, Fixed, and Marginal Cost and Output

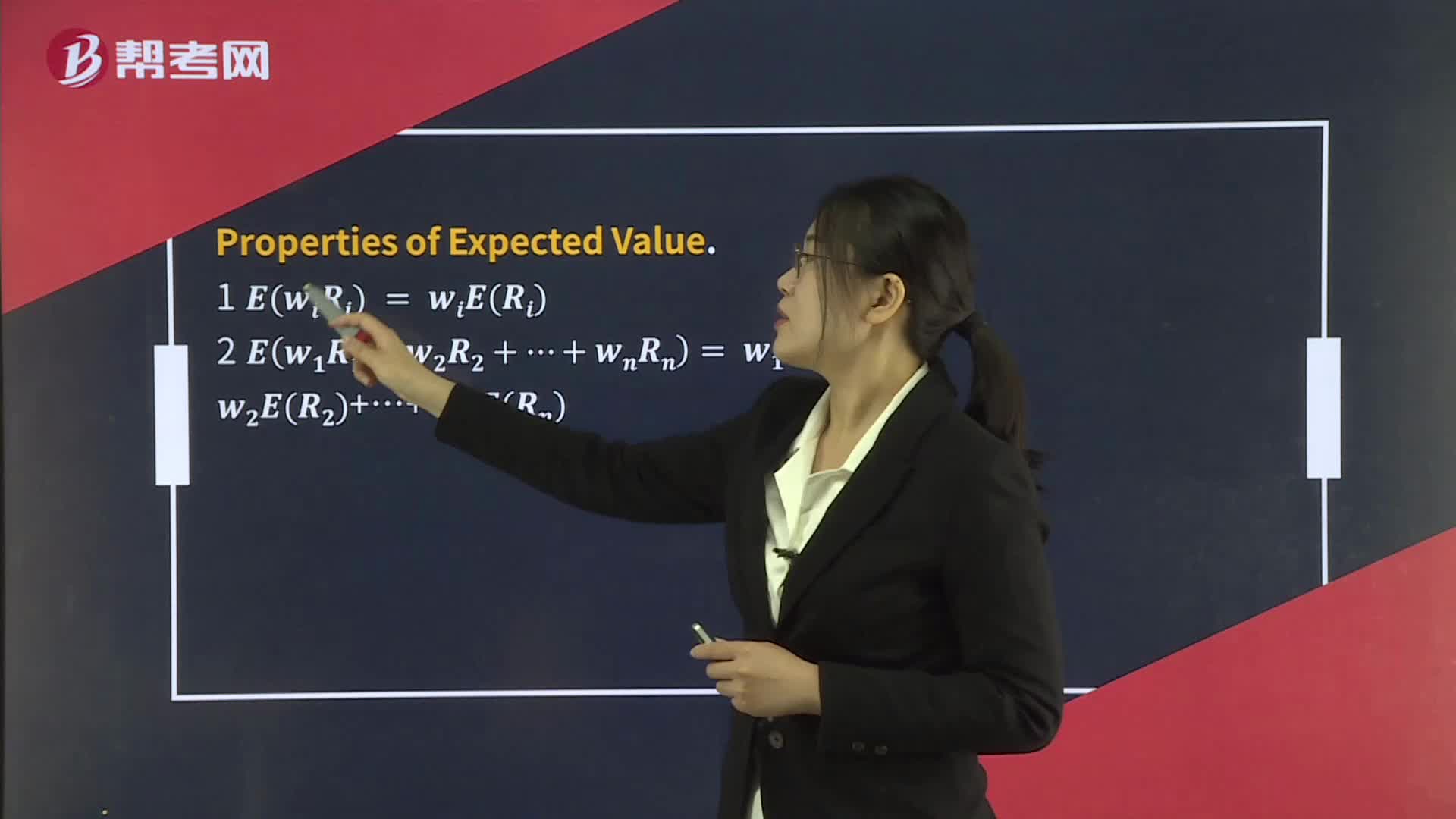

Multiplication Rule For Expected Value

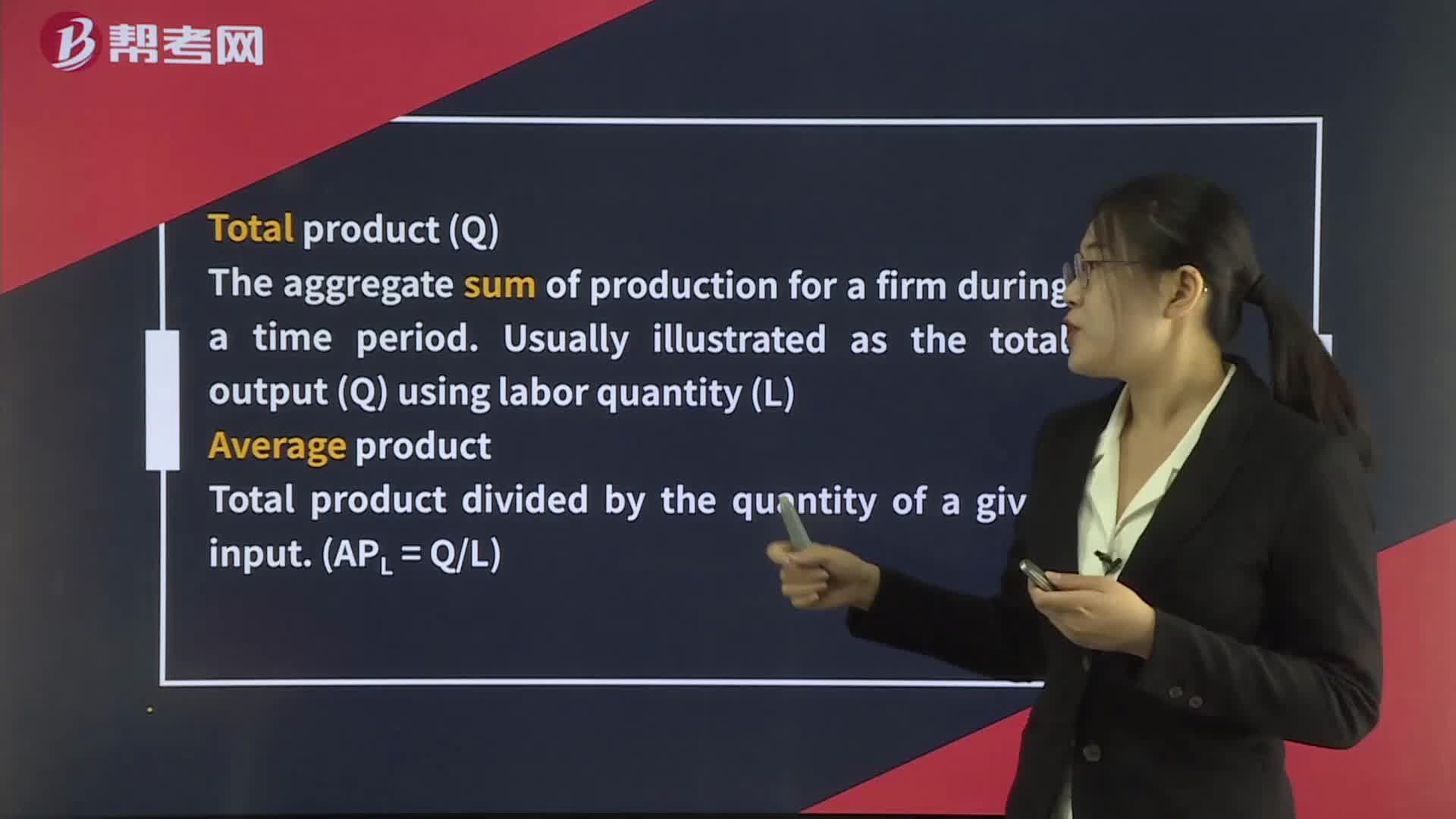

Total, Average, and Marginal Product of Labor

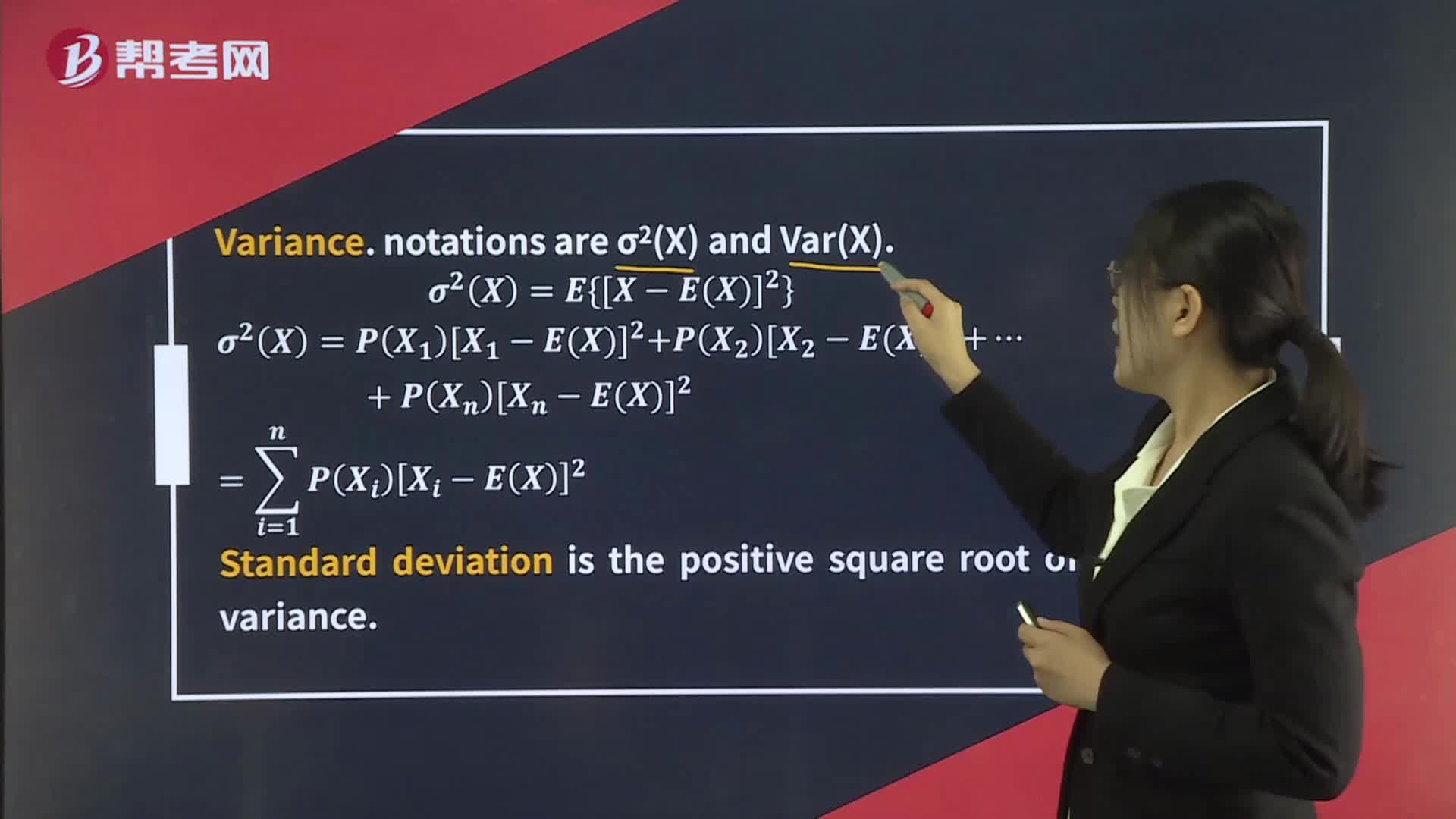

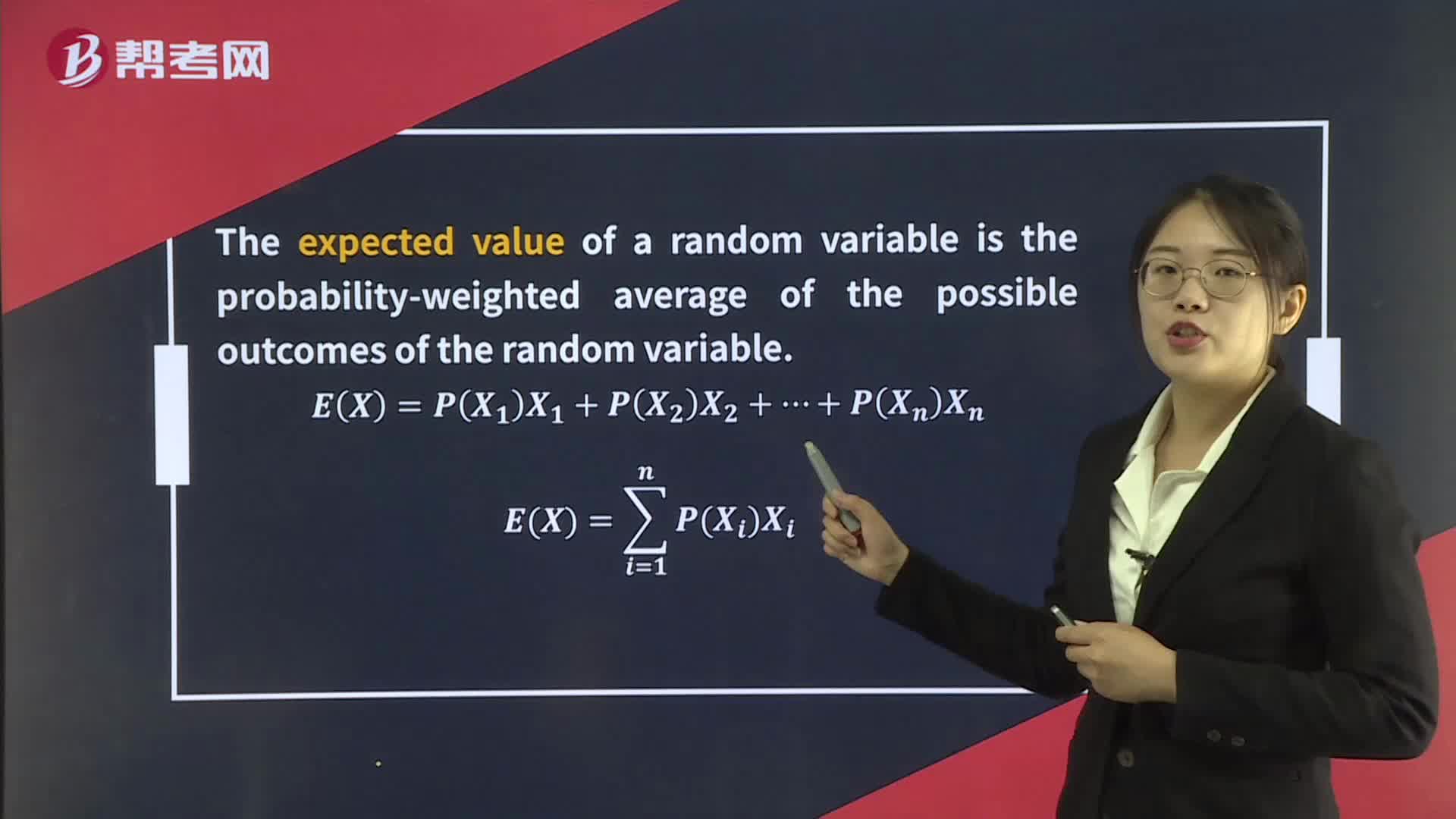

Expected Value and Variance

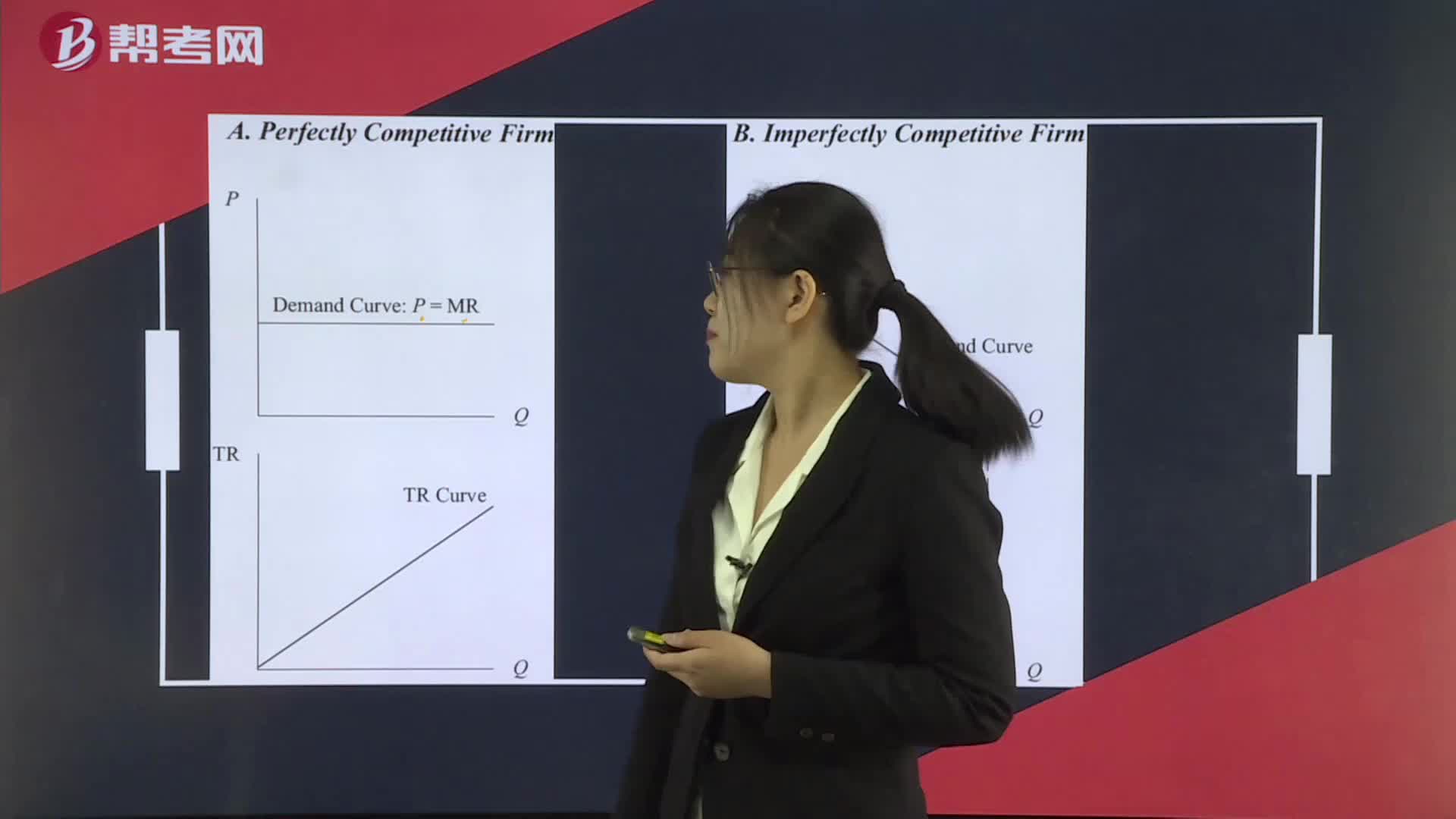

Revenue under Conditions of Perfect and Imperfect Competition

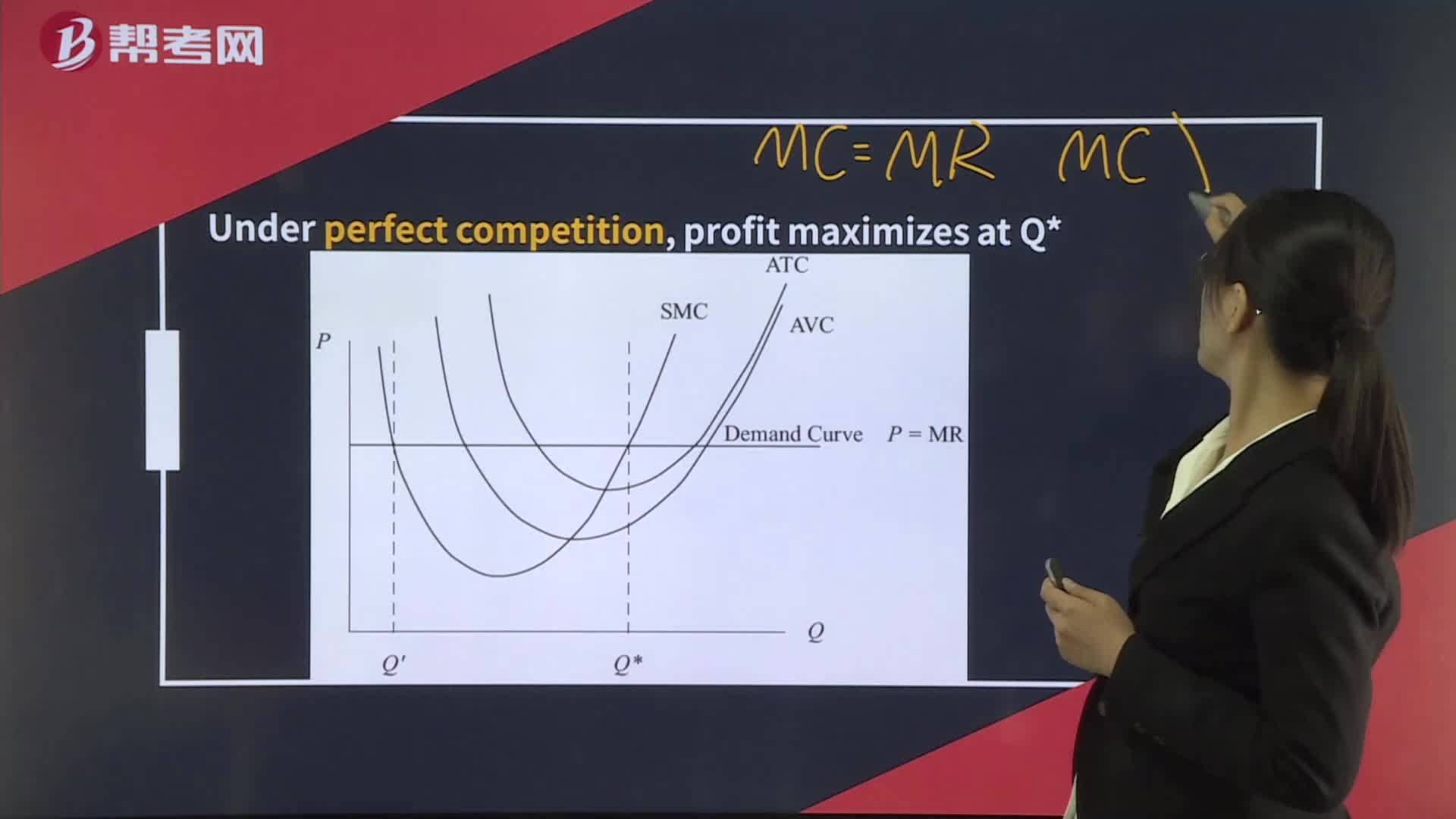

Profit-Maximization, Breakeven, and Shutdown Points of Production

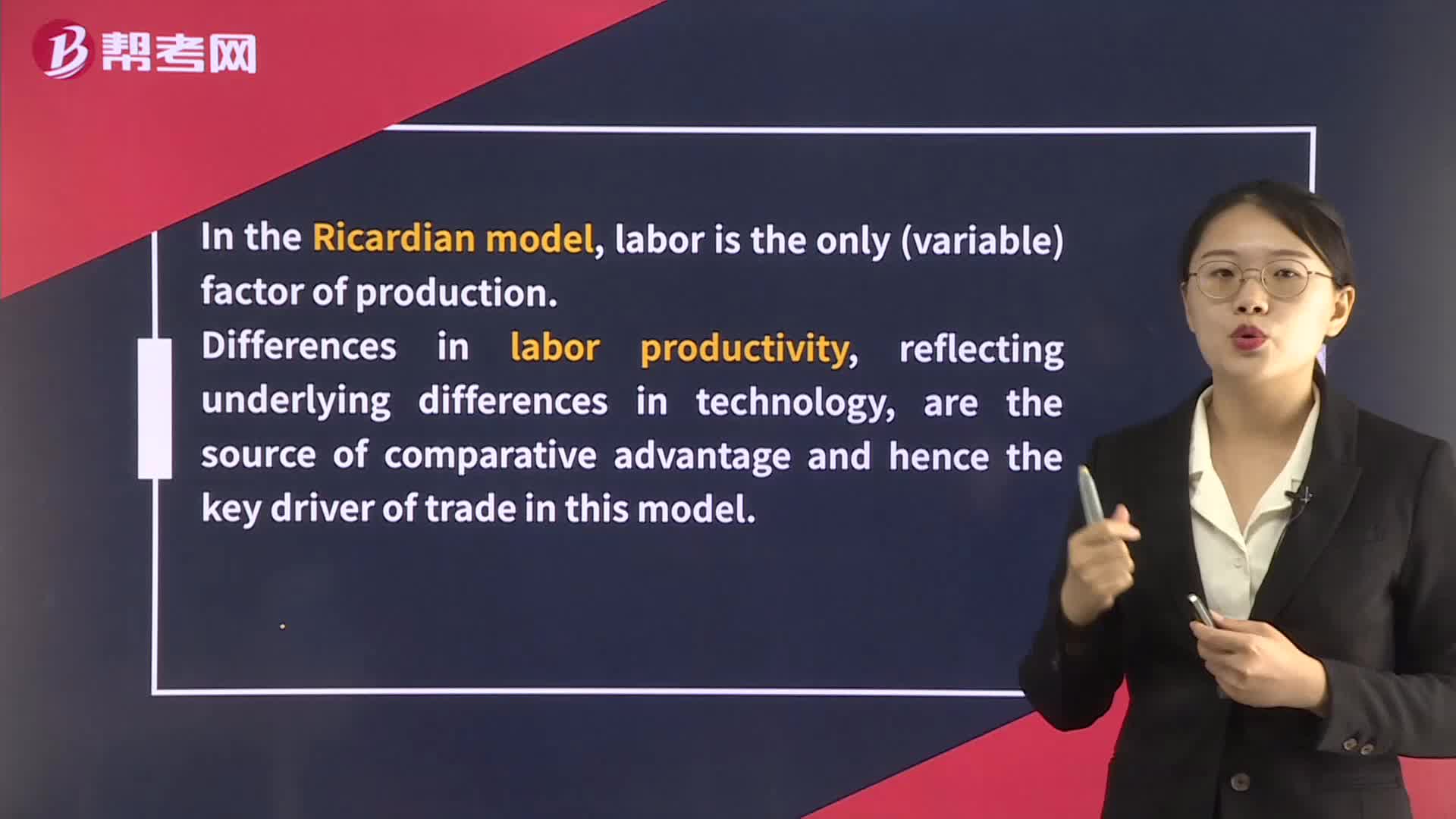

Ricardian and Heckscher–Ohlin Models of Comparative Advantage

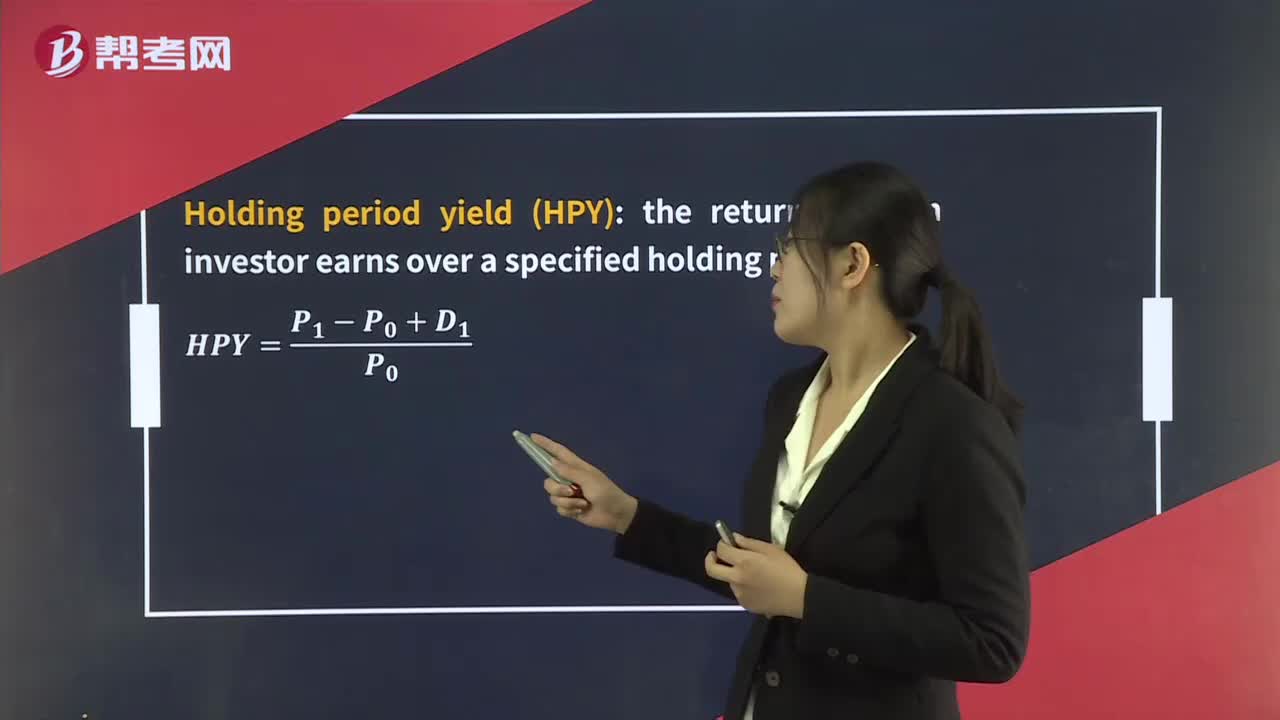

Money-Weighted Rate of Return & Time-Weighted Rate of Return

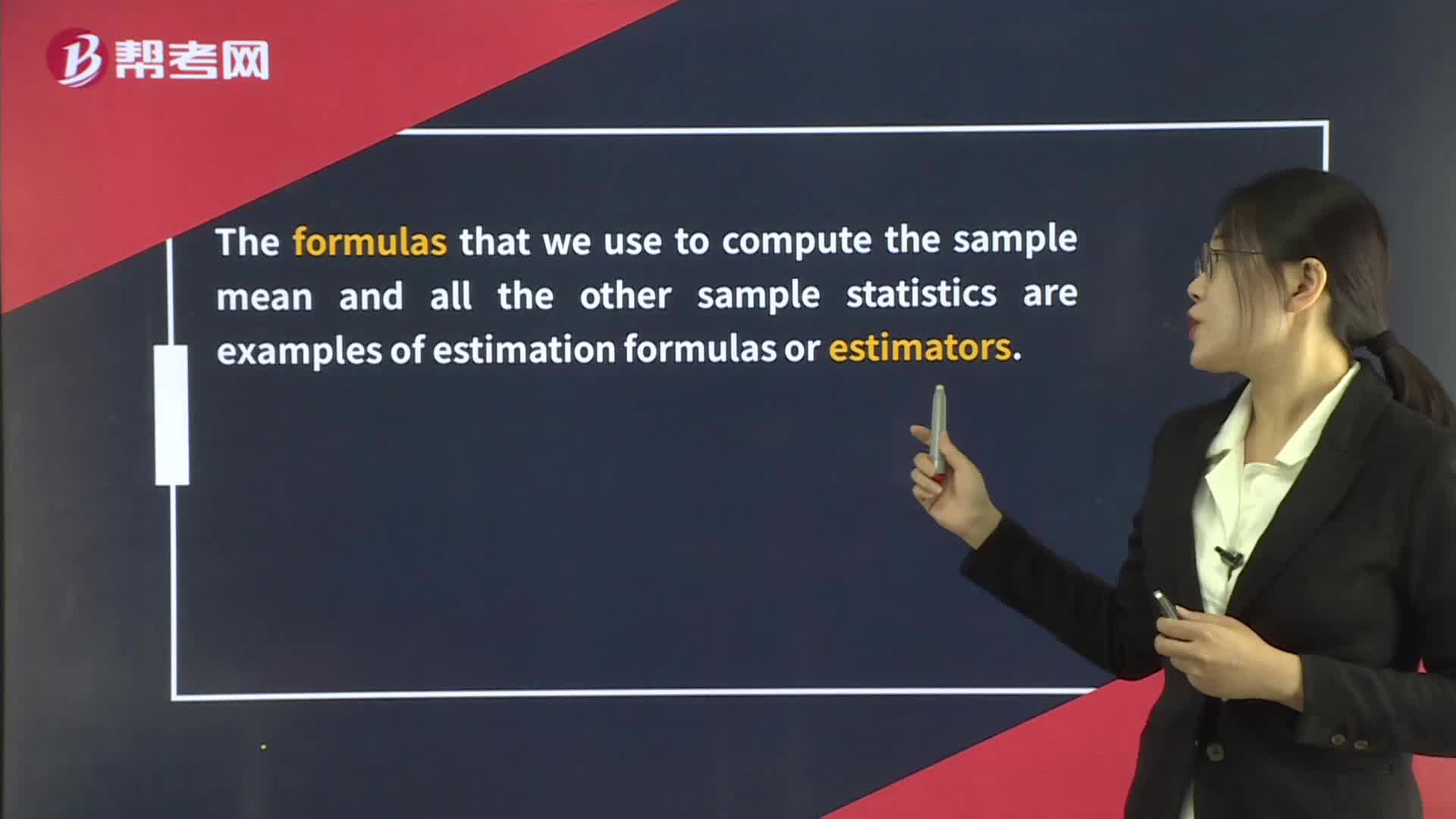

Point and Interval Estimates of the Population Mean

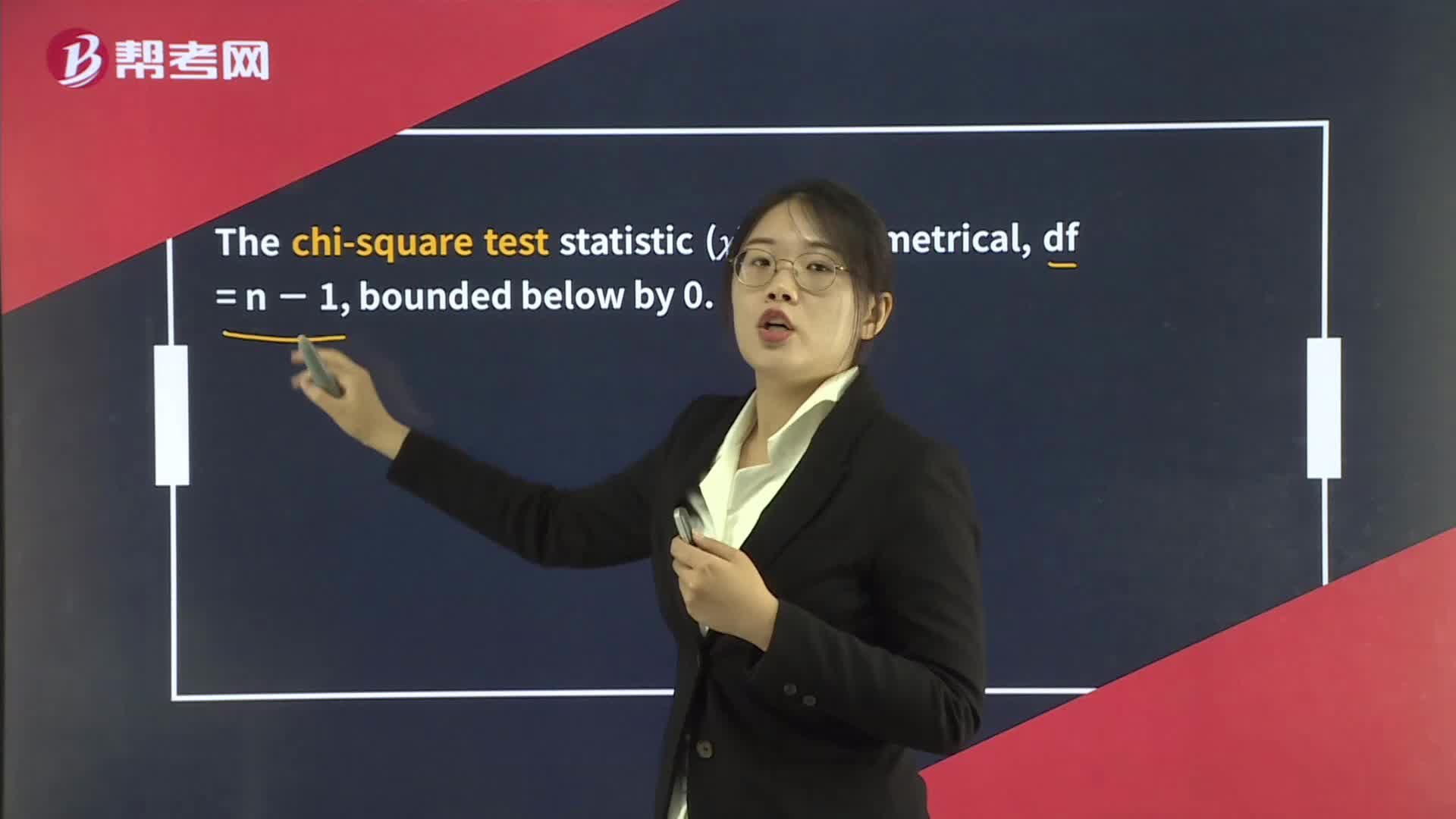

Hypothesis Tests Concerning Variance

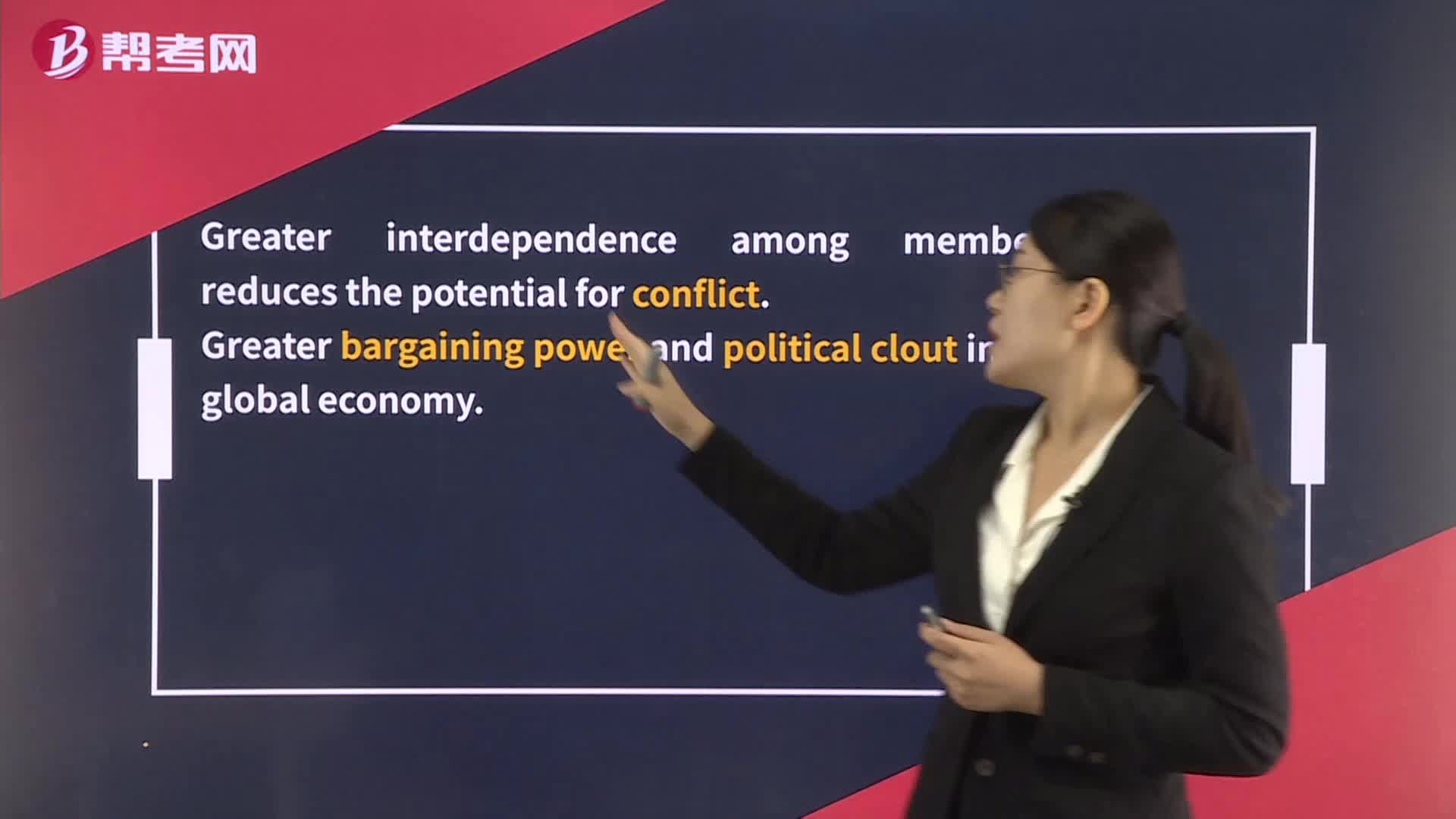

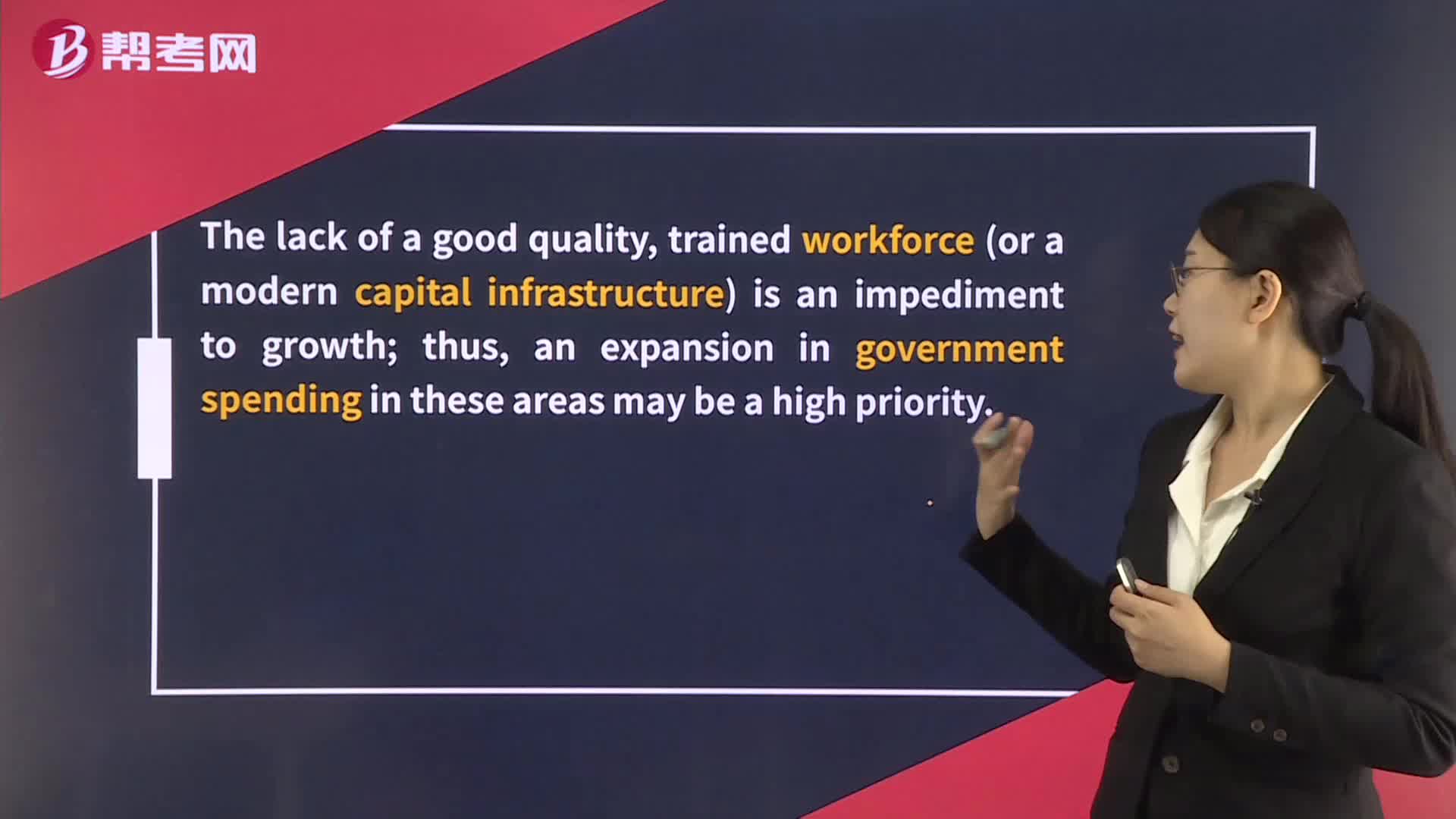

Benefits and Costs of Regional Trading Areas

09:33

09:33

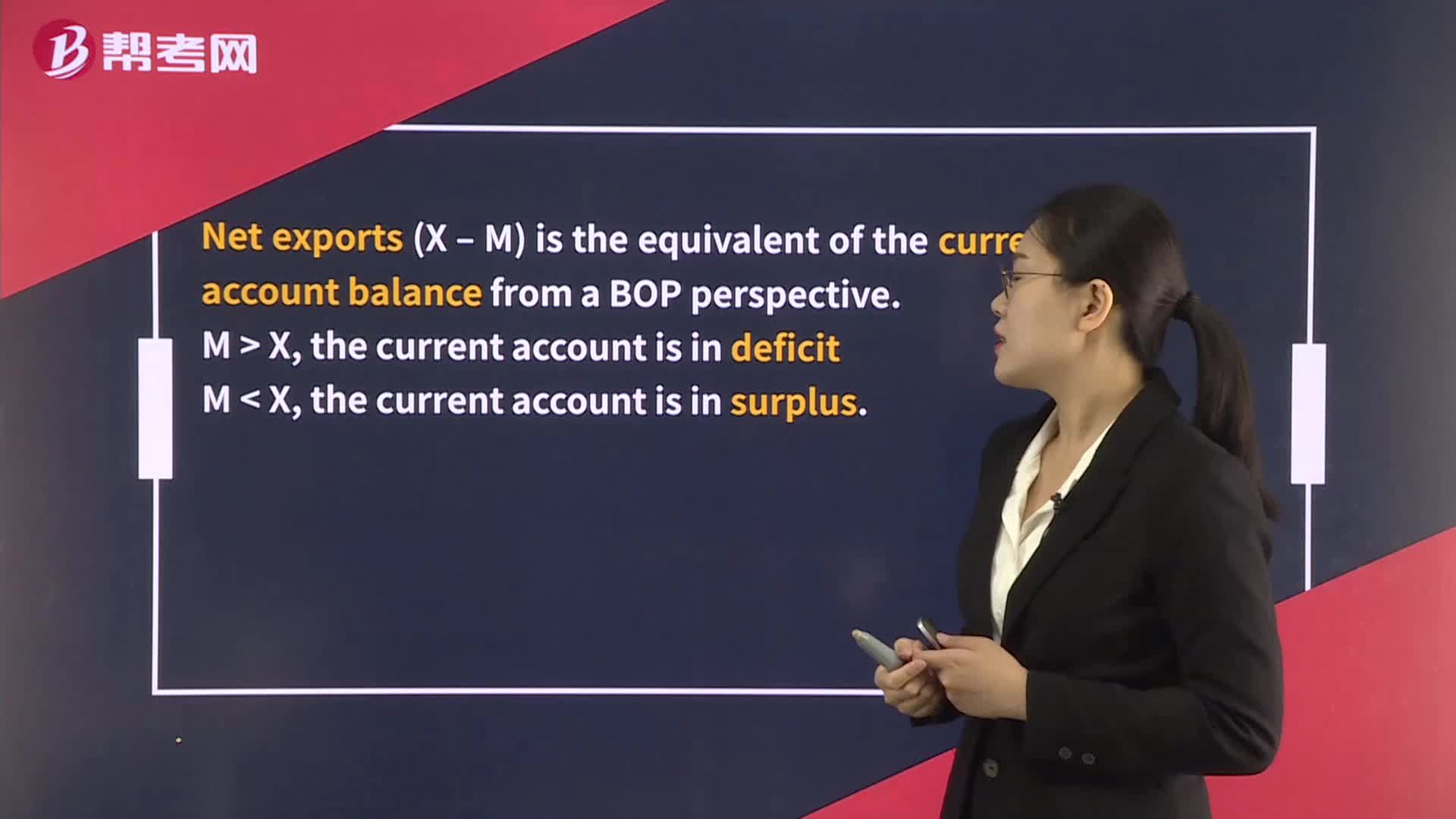

National Economic Accounts and the Balance of Payments:where:SpC–Sg.productive resources and its ability to repay its liabilities.Current

04:21

04:21

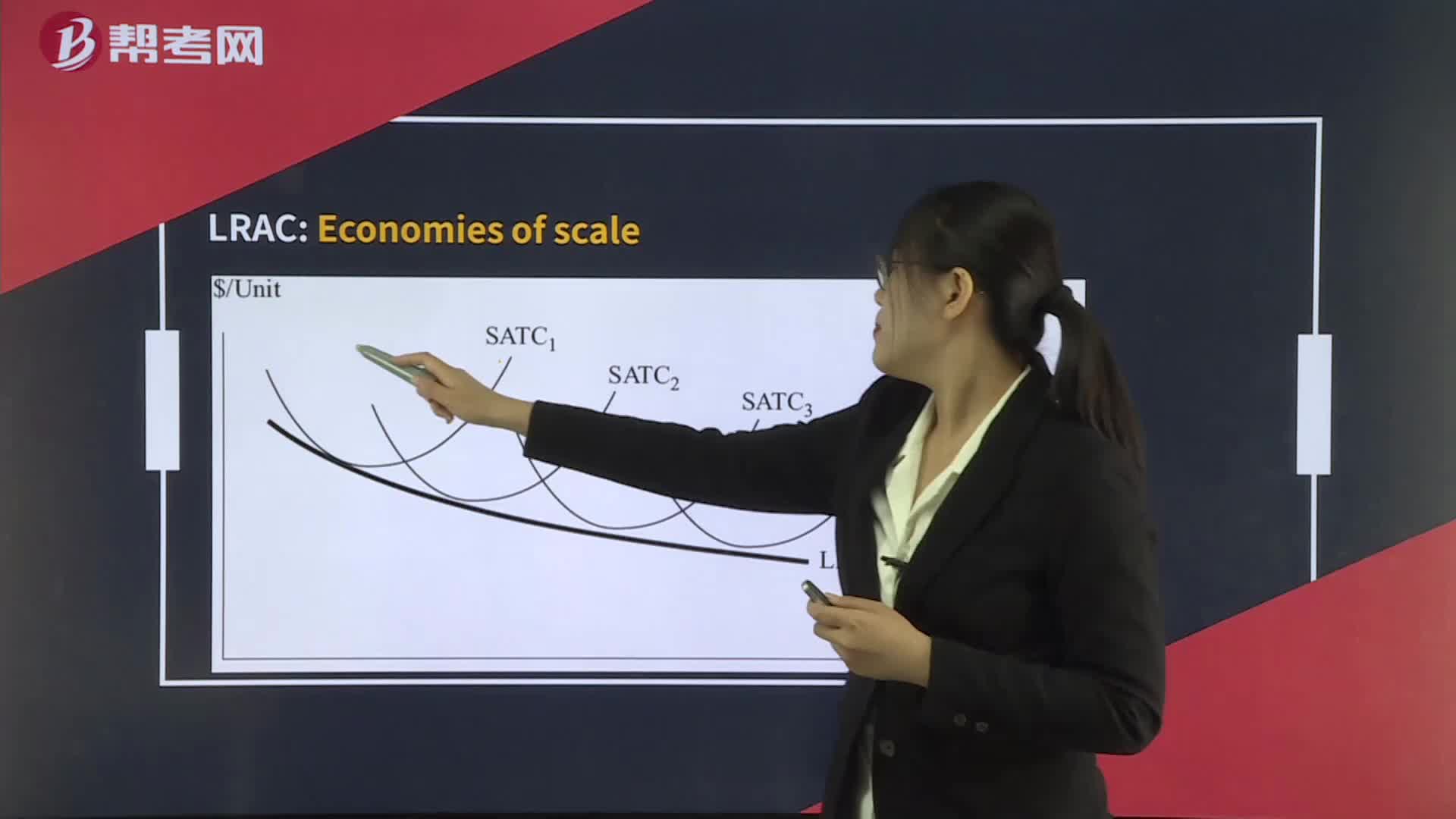

Economies of Scale and Diseconomies of Scale:as the firm increases its output:size under perfect competition over the long run.

03:09

03:09

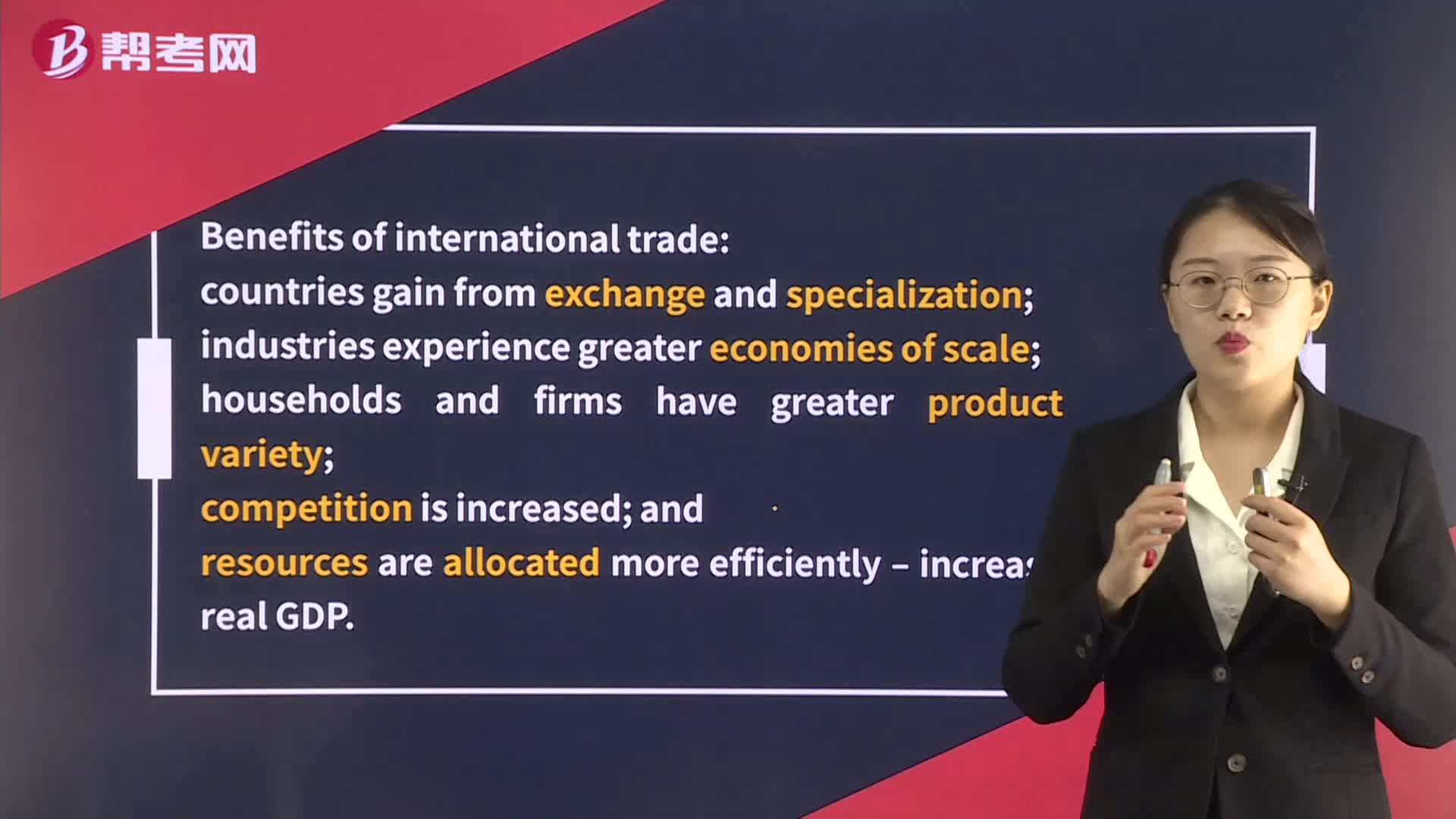

Benefits and Costs of International Trade:Benefits and Costs of International Trade:households and firms have greater product variety;of jobs in developed countries as a result of import competition.

02:22

02:22

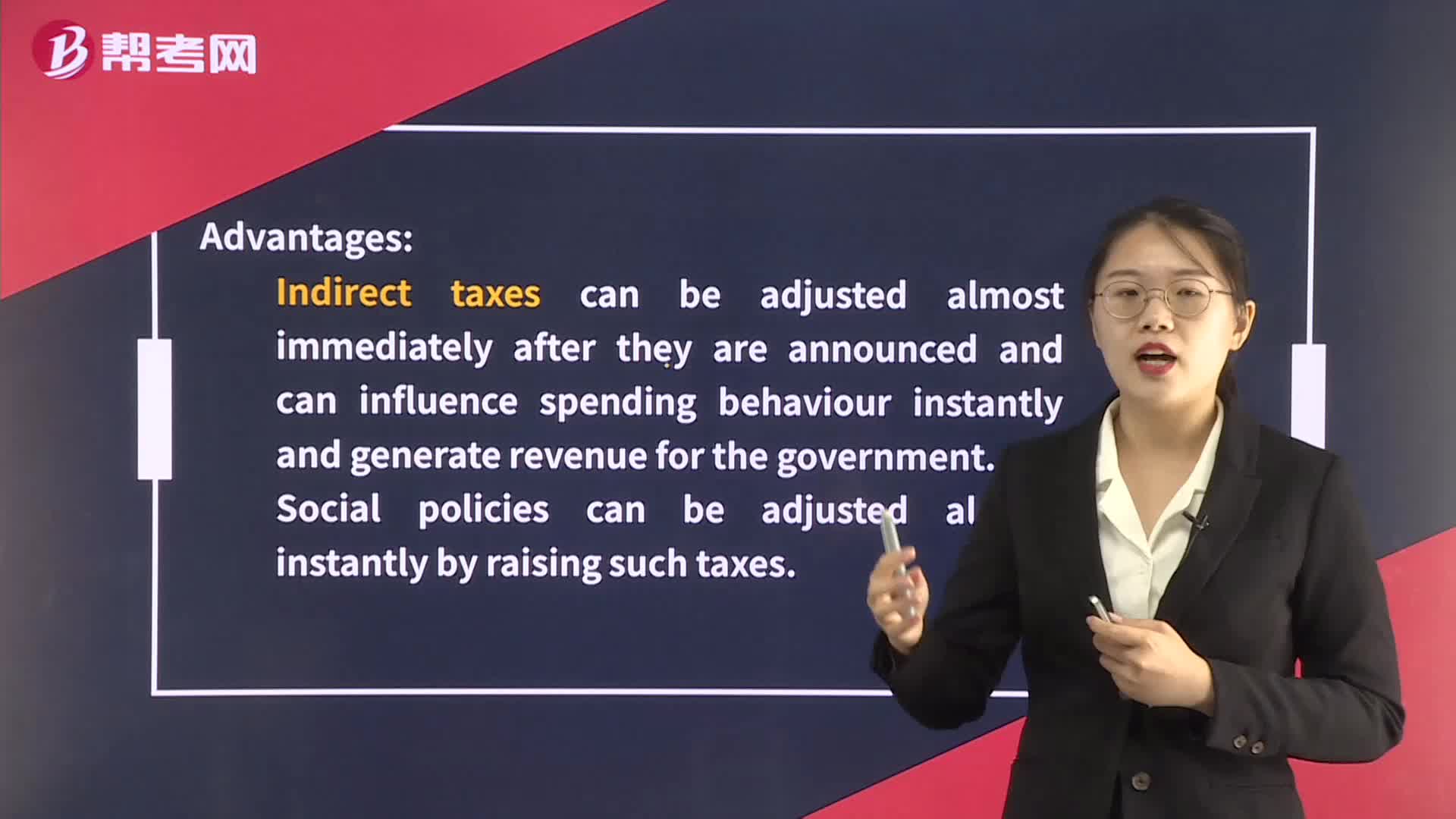

The Advantages and Disadvantages of Using the Different Tools of Fiscal Policy:Different Tools of Fiscal Policy:DirectCapitalpowerful as the direct effects.

04:28

04:28

Factors Influencing the Mix of Fiscal and Monetary Policy:Monetary Policy;by the political context.:Both fiscal and monetary policies suffer from;lack of precise knowledge of where:studyNoaccommodation.

16:32

16:32

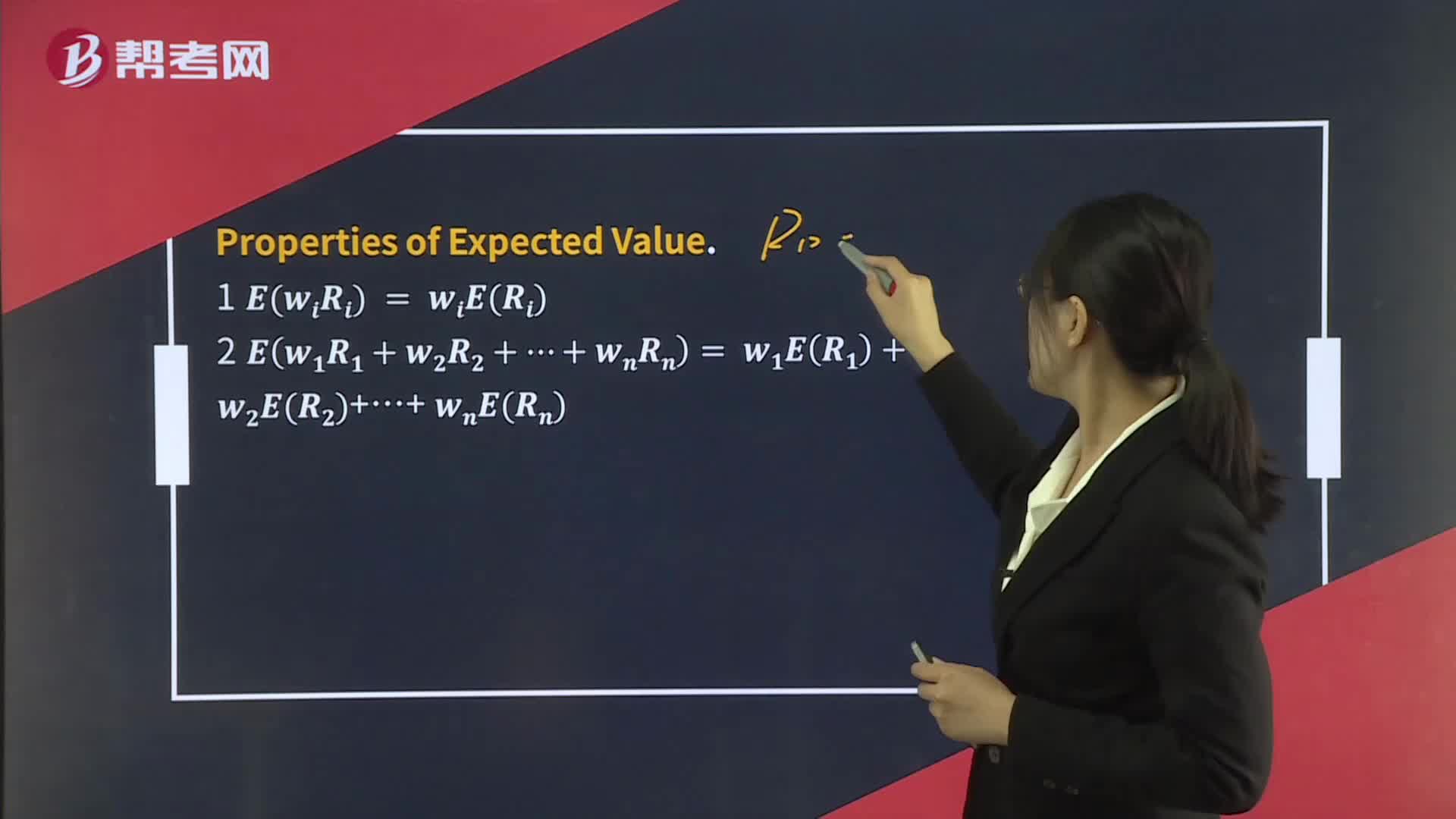

Portfolio Expected Return and Variance of Return:= 8112 = 9. Thus:RjB.C.FirstEXY = EXEY

03:04

03:04

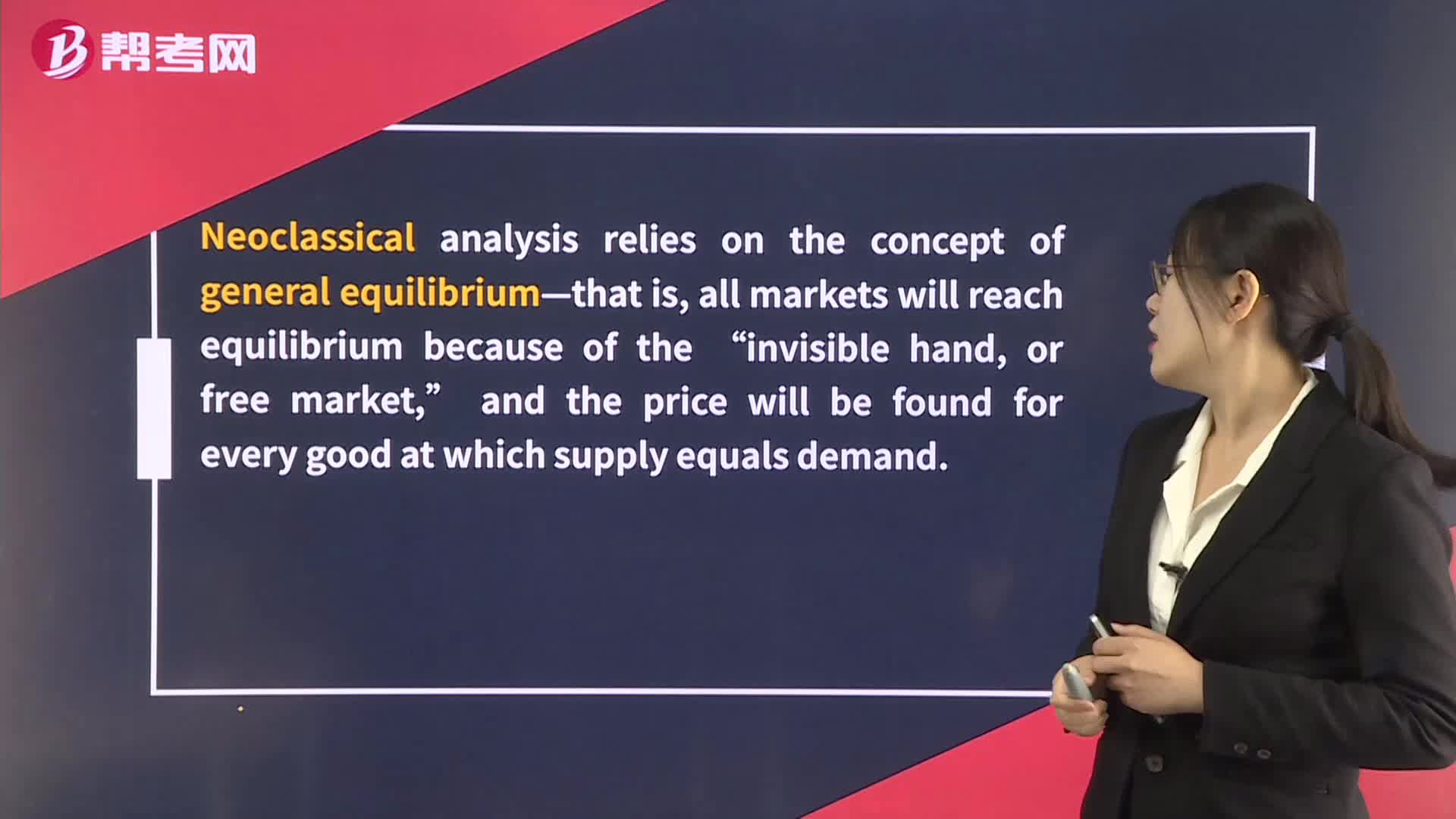

Theories of the Business Cycle - Neoclassical and Austrian Schools:hand,every good at which supply equals demand.:schoolto do in the recession phase is to allow the necessary market adjustment to take place as quickly as possible.

07:44

07:44

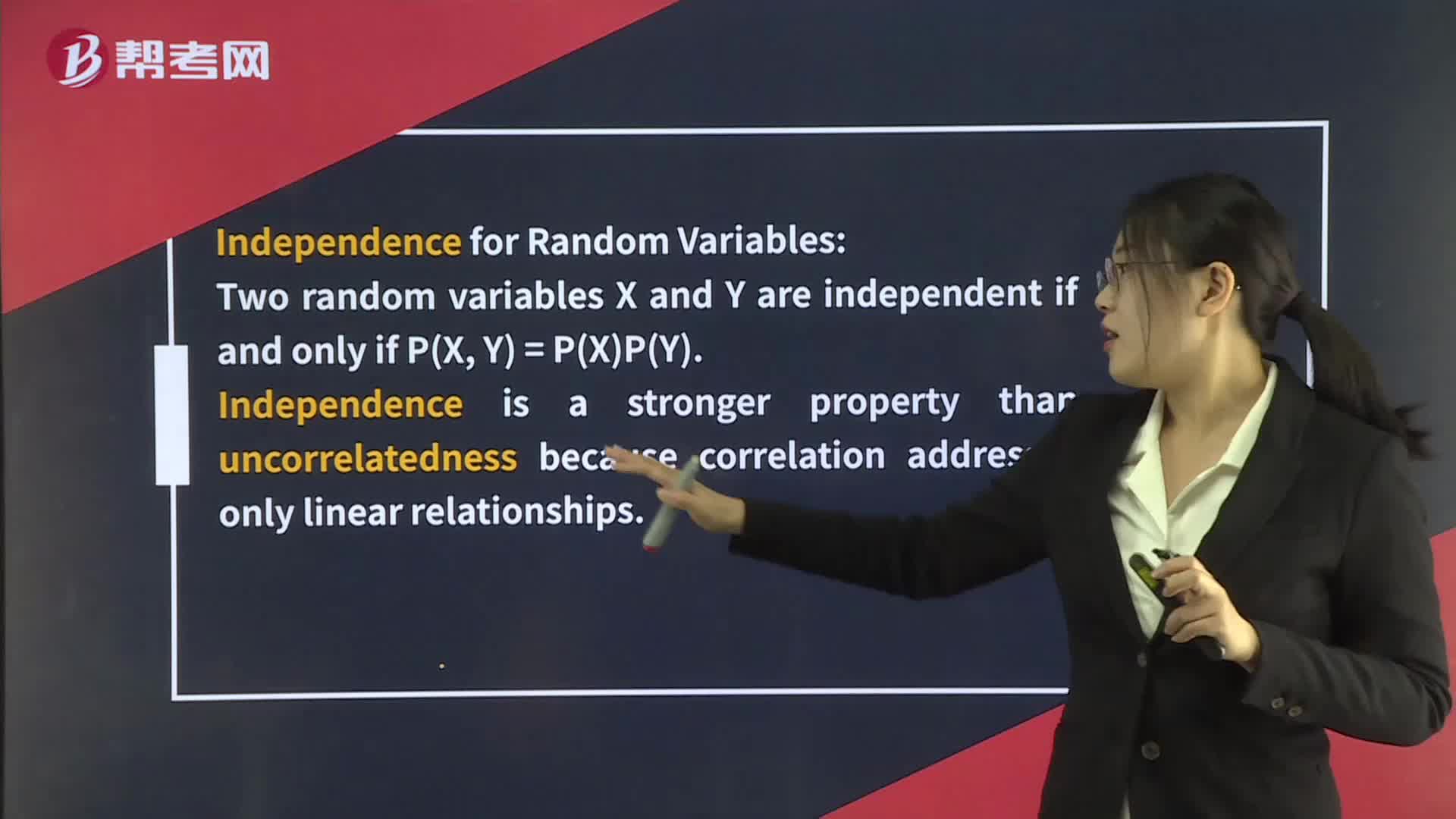

Expected Value & Variance:Expected Value Variance:million.,B.,C.,$32.40 million.,600.

00:53

00:53

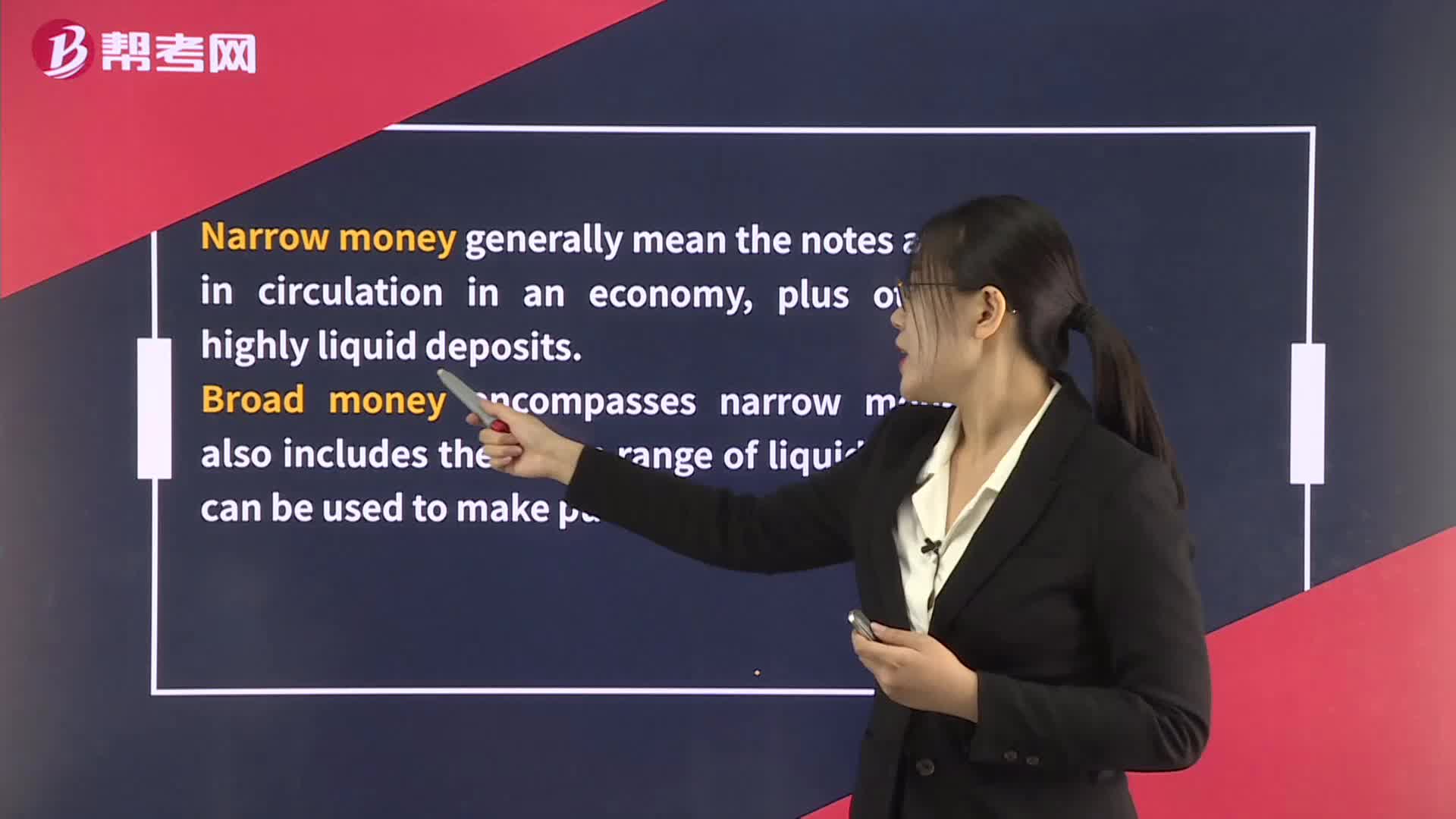

Definitions of Money:entire range of liquid assets that can be used to make purchases.

04:12

04:12

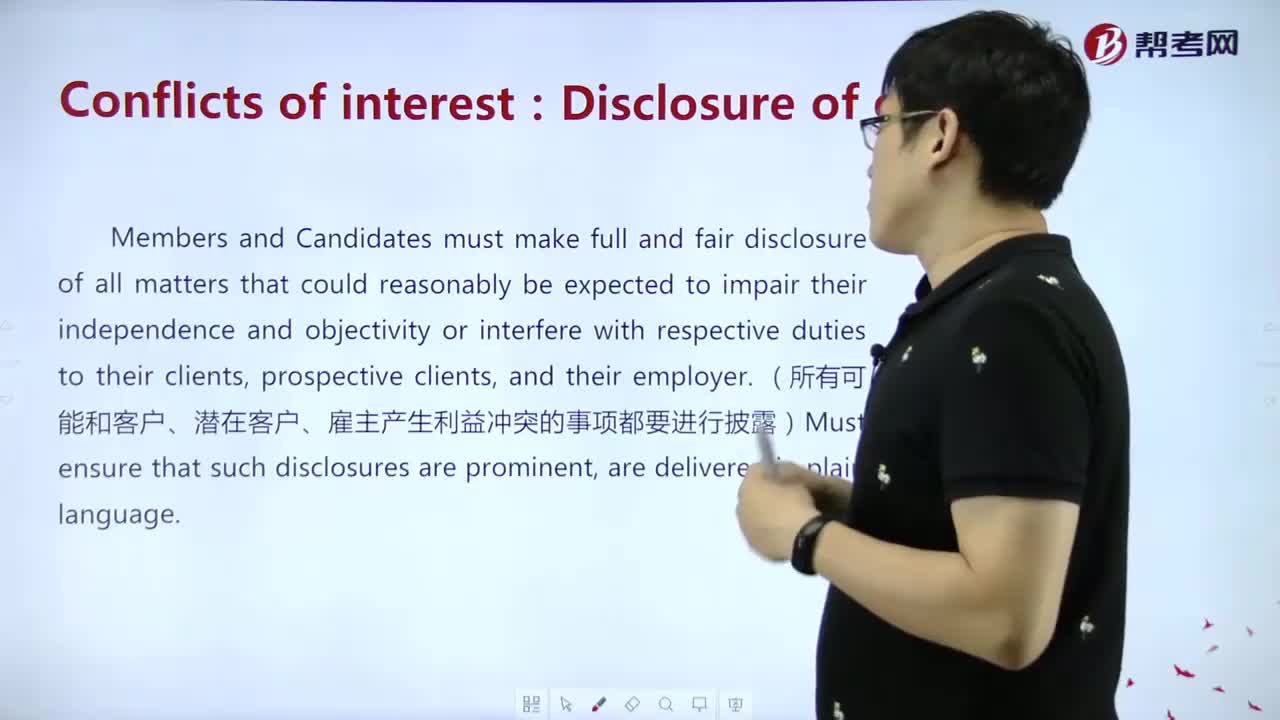

Why members and candidates must make disclosure of all matters ?:and their employer. (所有可能和客戶、潛在客戶、雇主產(chǎn)生利益沖突的事項(xiàng)都要進(jìn)行披露)Must ensure that such disclosures are prominent,必須披露)The best practice is to assign another to follow up the company.;

11:00

11:00

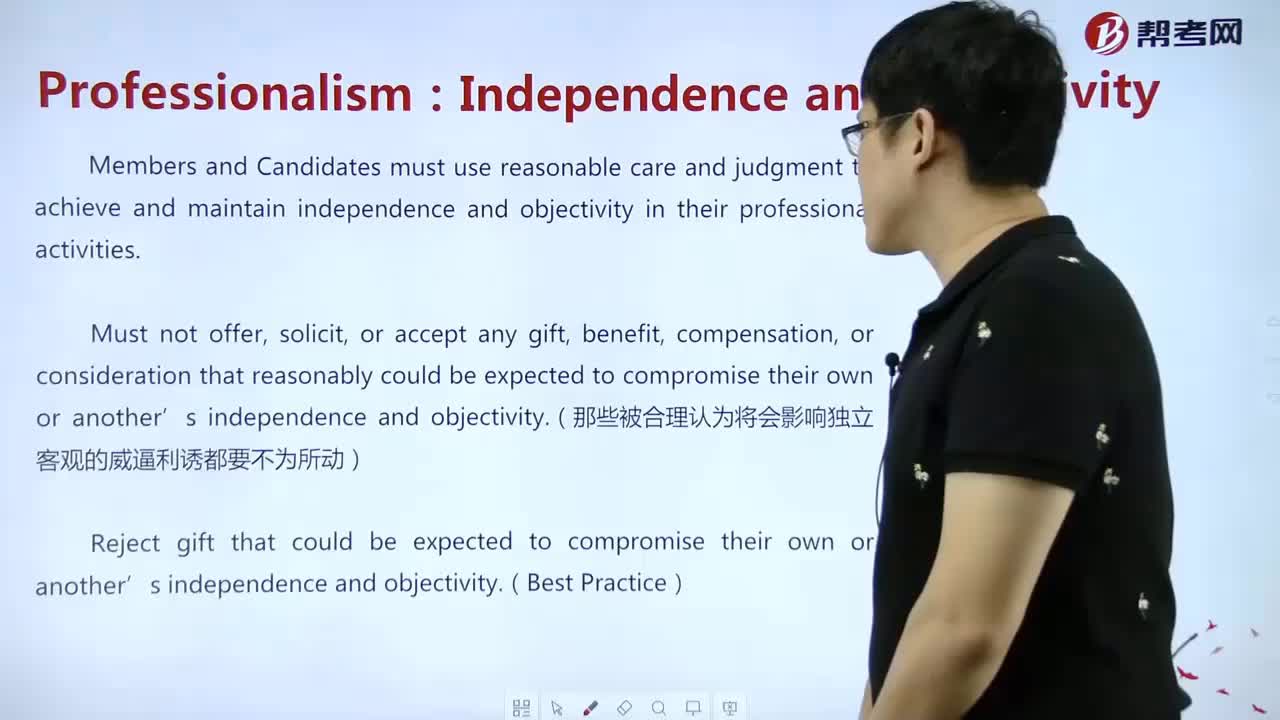

What's the meaning of independence and objectivity in professionalism?:or consideration that reasonably could be expected to compromise their own or another’s independence and objectivity.(那些被合理認(rèn)為將會(huì)影響?yīng)毩⒖陀^的威逼利誘都要不為所動(dòng)),但在他人眼中會(huì)影響?yīng)毩⑿砸膊恍校┛赡艿脑捠孪扰督o雇主告訴雇主是為了引起雇主的同意

06:50

06:50

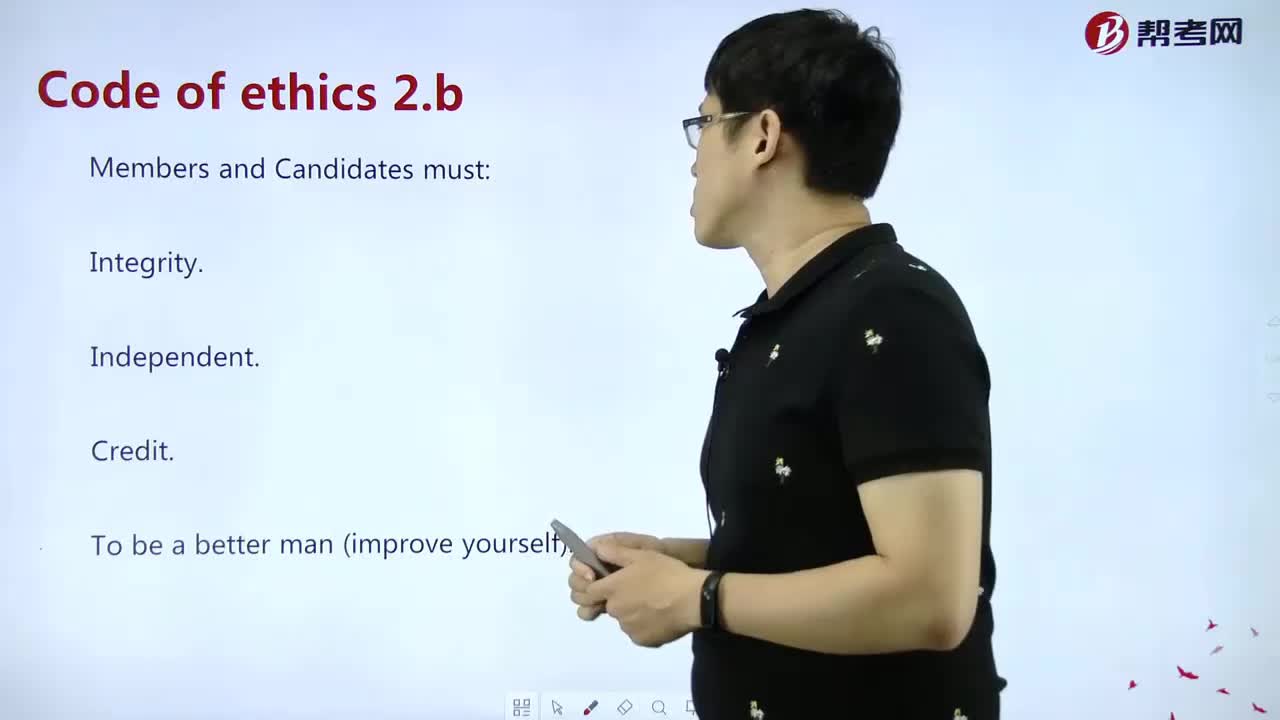

How to understand the Code of ethics and trust in the investment profession?:I,Professionalism:II:IIIIVVVIVIIResponsibilities as a CFA member or candidate