下載億題庫APP

聯(lián)系電話:400-660-1360

下載億題庫APP

聯(lián)系電話:400-660-1360

請謹(jǐn)慎保管和記憶你的密碼,以免泄露和丟失

請謹(jǐn)慎保管和記憶你的密碼,以免泄露和丟失

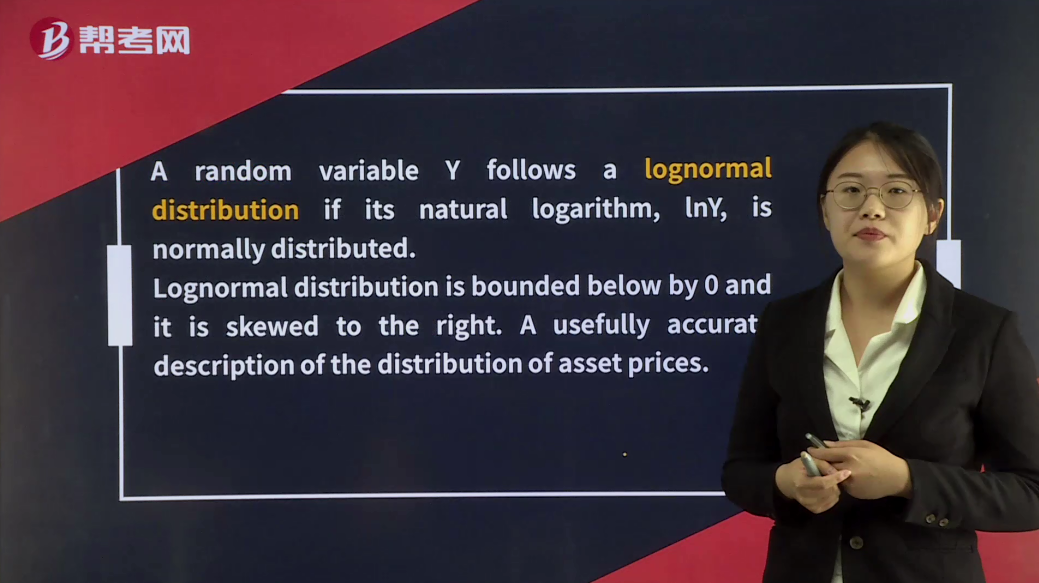

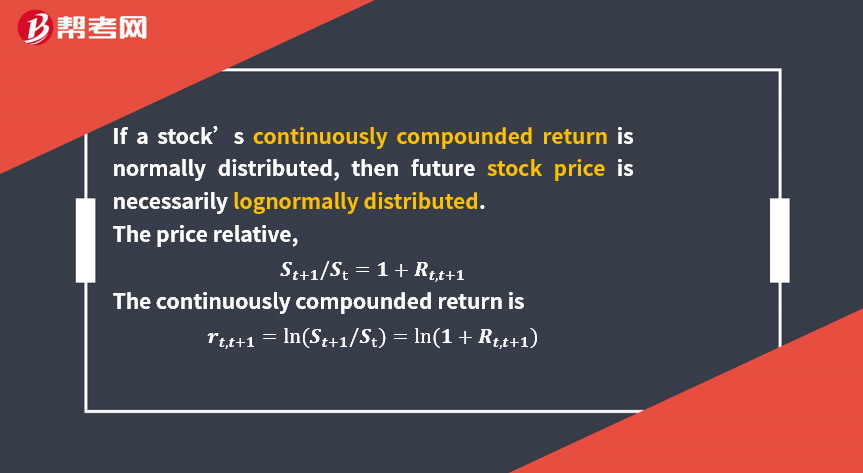

The Lognormal Distribution

A random variable Y follows a lognormal distribution if its natural logarithm, lnY, is normally distributed.

Lognormal distribution is bounded below by 0 and it is skewed to the right. A usefully accurate description of the distribution of asset prices.

[Practice Problems] In contrast to normal distributions, lognormal distributions:

A. are skewed to the left.

B. have outcomes that cannot be negative.

C. are more suitable for describing asset returns than asset prices.

[Solutions] B

By definition, lognormal random variables cannot have negative values.

191

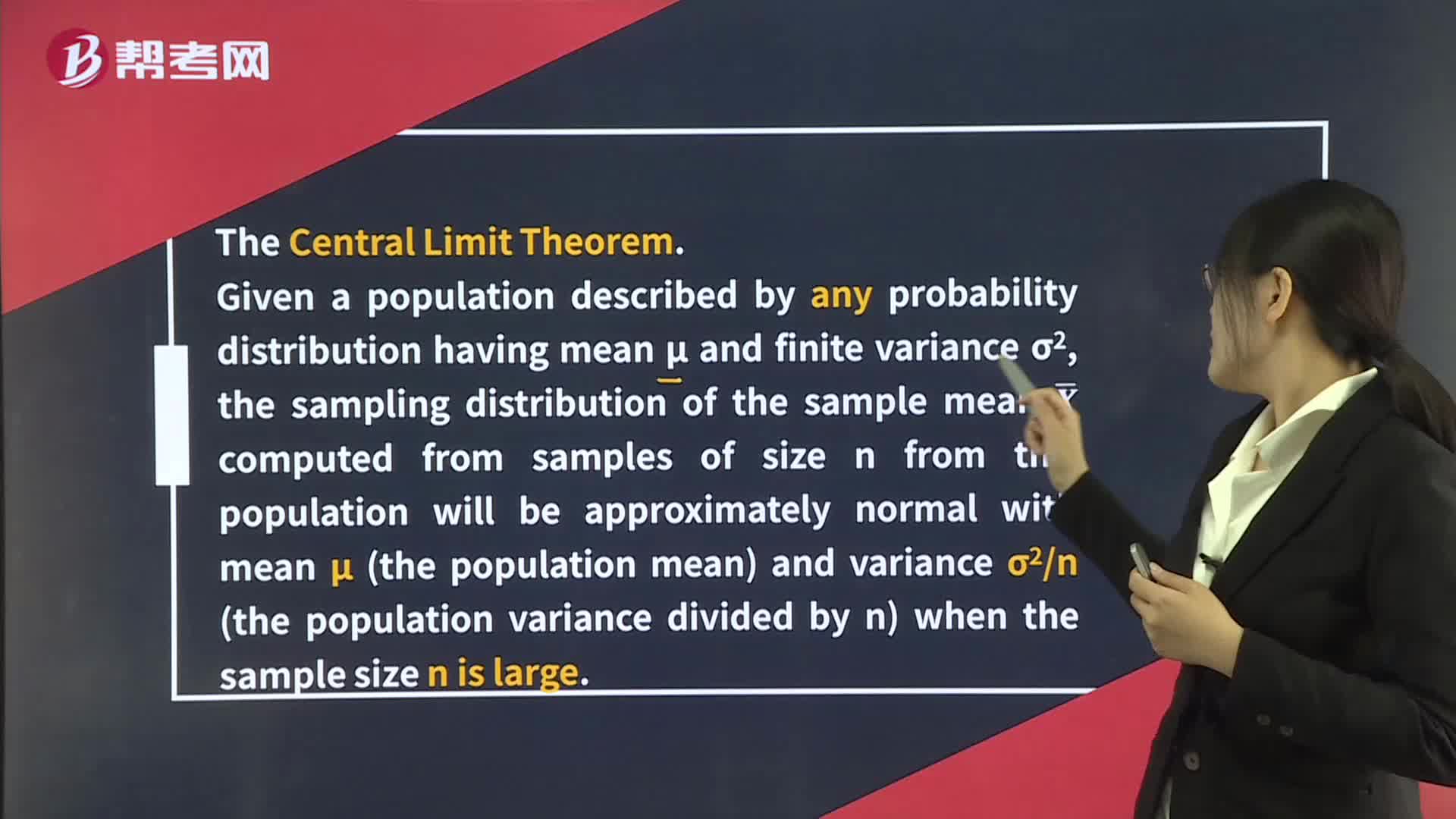

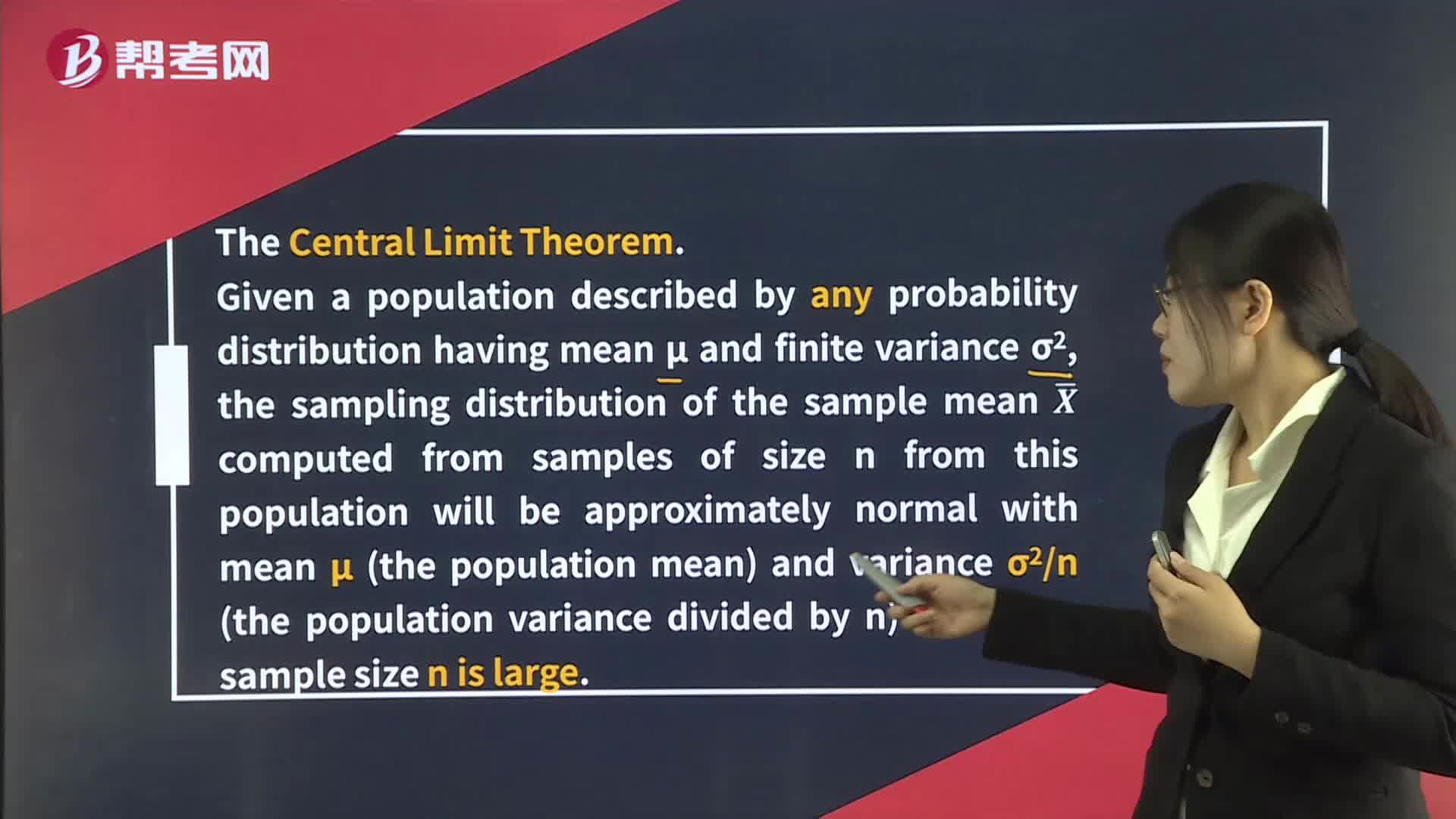

191Distribution of the Sample Mean:[Practicewhen the sample size is large.

168

168Distribution of the Sample Mean:The Central:[PracticeB.C.when the sample size is large.

599

599The Normal Distribution:μ;indicated as X ~ Nμ:Approximately 99% fall in μ ± 2.58σ.[PracticemeanNZ corresponding to 8% must equal 50%. So P8% ≤ Portfolio return ≤ 11% = 0.5832 – 0.50 = 0.0832 or approximately 8.3 percent.

微信掃碼關(guān)注公眾號

獲取更多考試熱門資料