下載億題庫APP

聯(lián)系電話:400-660-1360

下載億題庫APP

聯(lián)系電話:400-660-1360

請謹慎保管和記憶你的密碼,以免泄露和丟失

請謹慎保管和記憶你的密碼,以免泄露和丟失

Long-Run Equilibrium in Perfectly Competitive Markets

微信截圖_1596683310606920200806111219995[1]20200806133833441.png)

The long-run marginal cost schedule is the perfectly competitive firm’s supply curve.

The firm’s demand schedule is the same as the firm’s marginal revenue and average revenue. The demand curve is perfectly elastic.

[Practice Problems] The demand schedule in a perfectly competitive market is given by P = 93 –

1.5Q (for Q ≤ 62) and the long-run cost structure of each company is:

Total cost: 256 + 2Q + 4Q2

Average cost: 256/Q + 2 + 4Q

Marginal cost: 2 + 8Q

New companies will enter the market at any price greater than: A. 8. B. 66. C. 81.

[Solutions] B

The long-run competitive equilibrium occurs where MC=AC = P for each company. Equating MC and AC implies 2 + 8Q=256/Q + 2 + 4Q. Solving for Q gives Q=8. Equating MC with price gives P=2 + 8Q=66. Any price above 66 yields an economic profit because P=MC > AC, so new companies will enter the market.

144

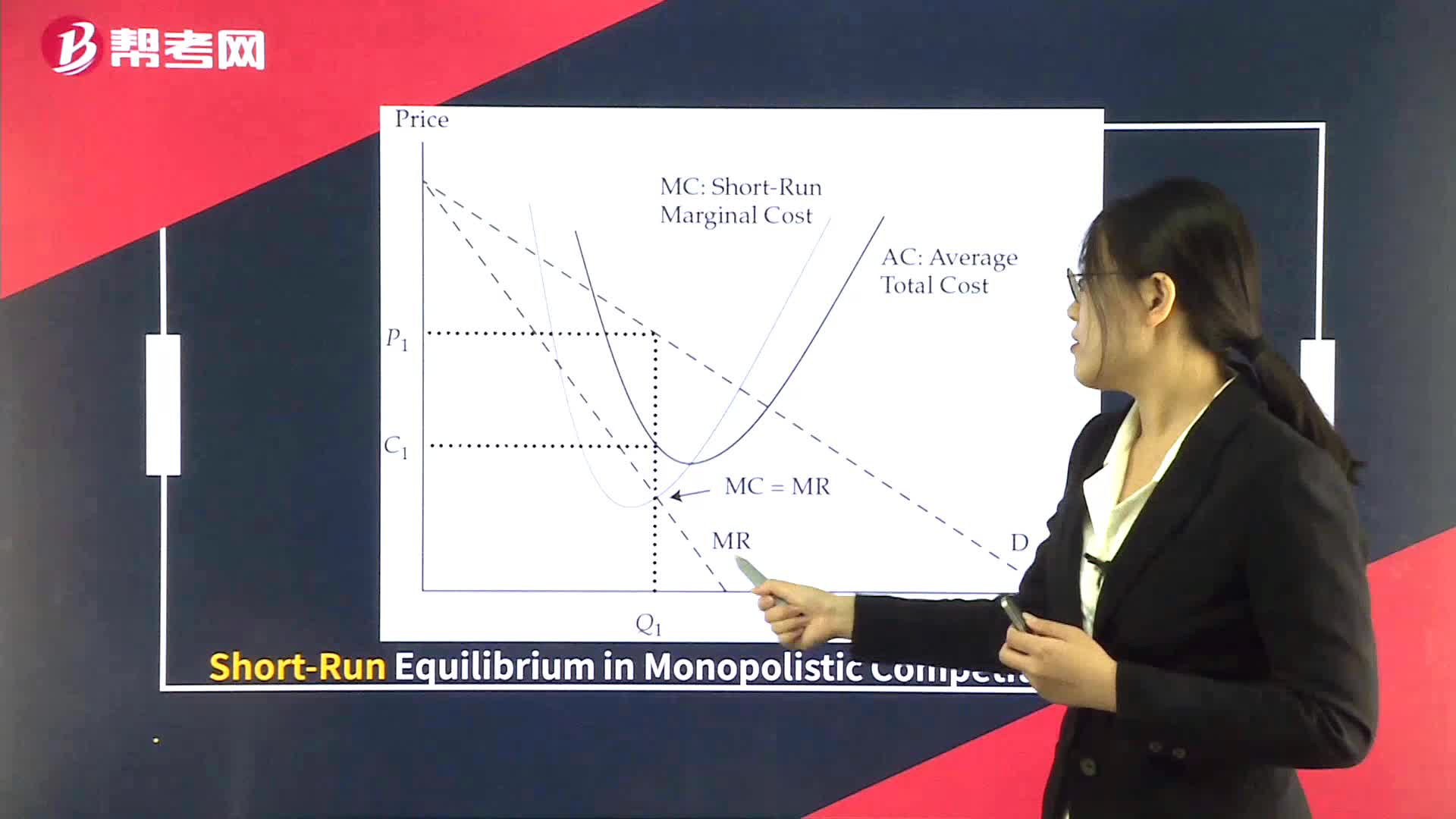

144Short-Run Equilibrium in Monopolistic Competition:π = TR – TC

177

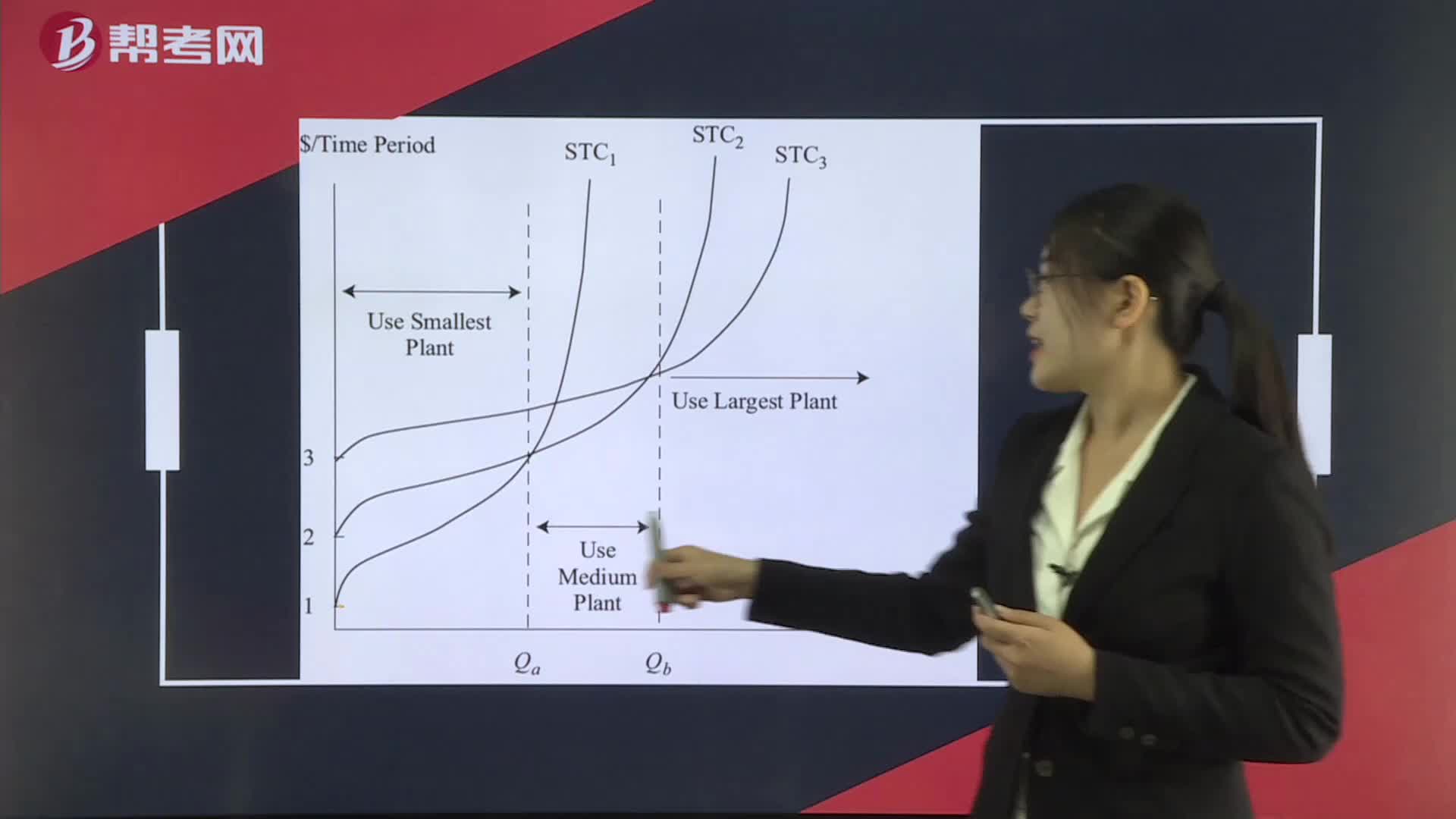

177Short- and Long-Run Cost Curves:Short-“and Long-Run Cost Curves”cost SATC curve and a corresponding long-runaverage total cost LRAC curve.

227

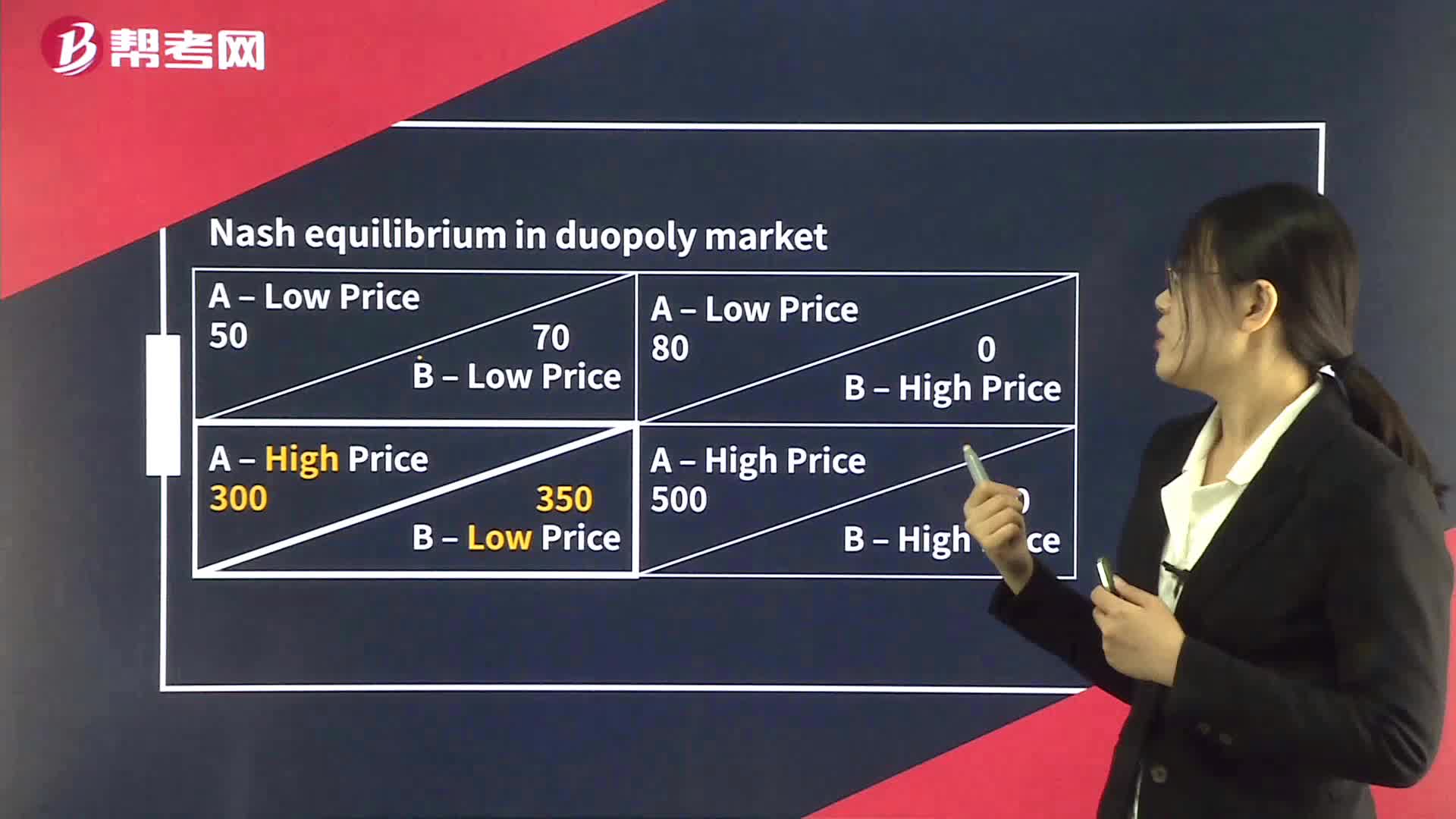

227Nash Equilibrium in Oligopoly Market:be willing to charge high prices.

微信掃碼關(guān)注公眾號

獲取更多考試熱門資料