Monte Carlo Simulation

幫考網(wǎng)校2020-08-06 18:24:24

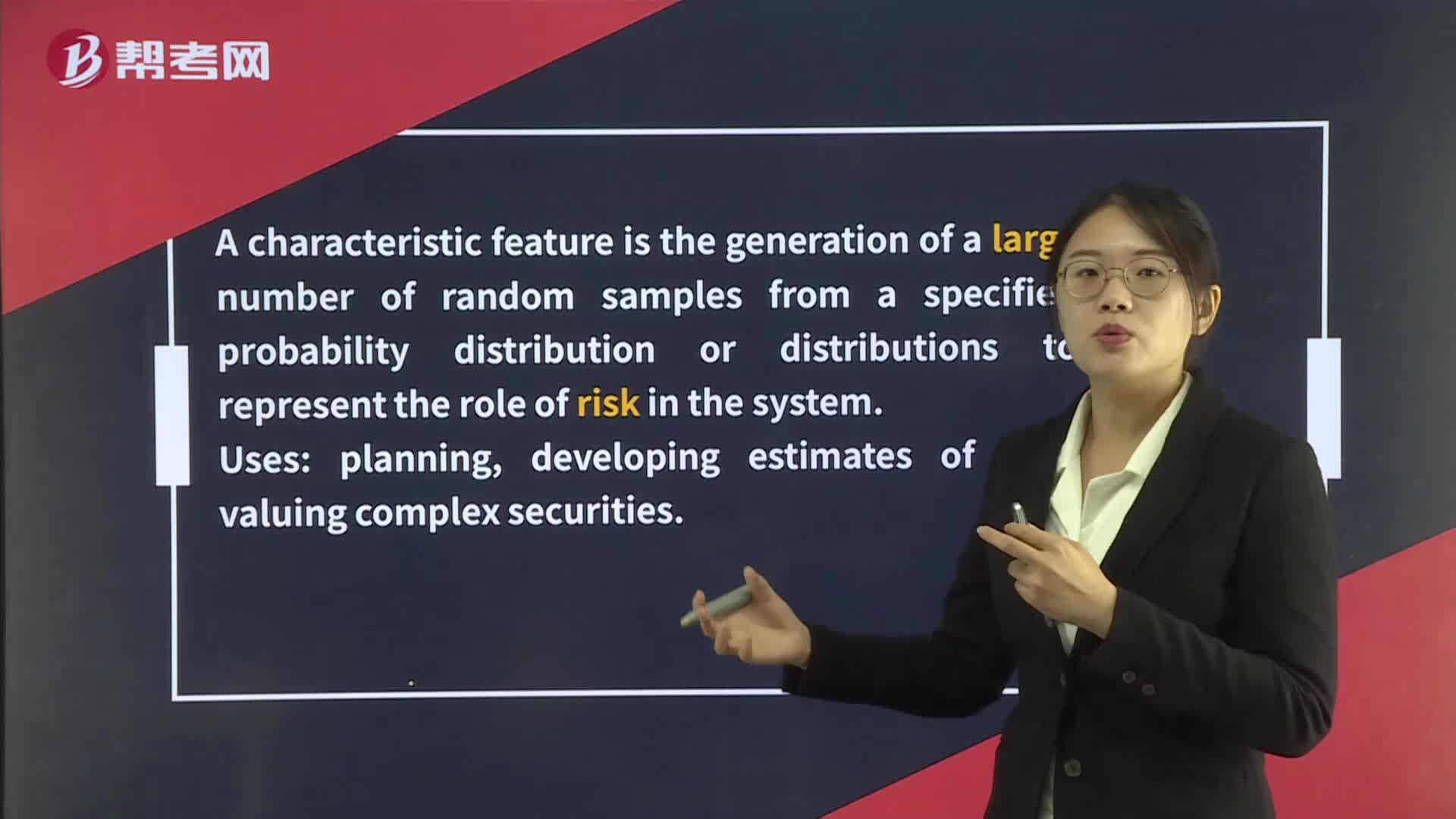

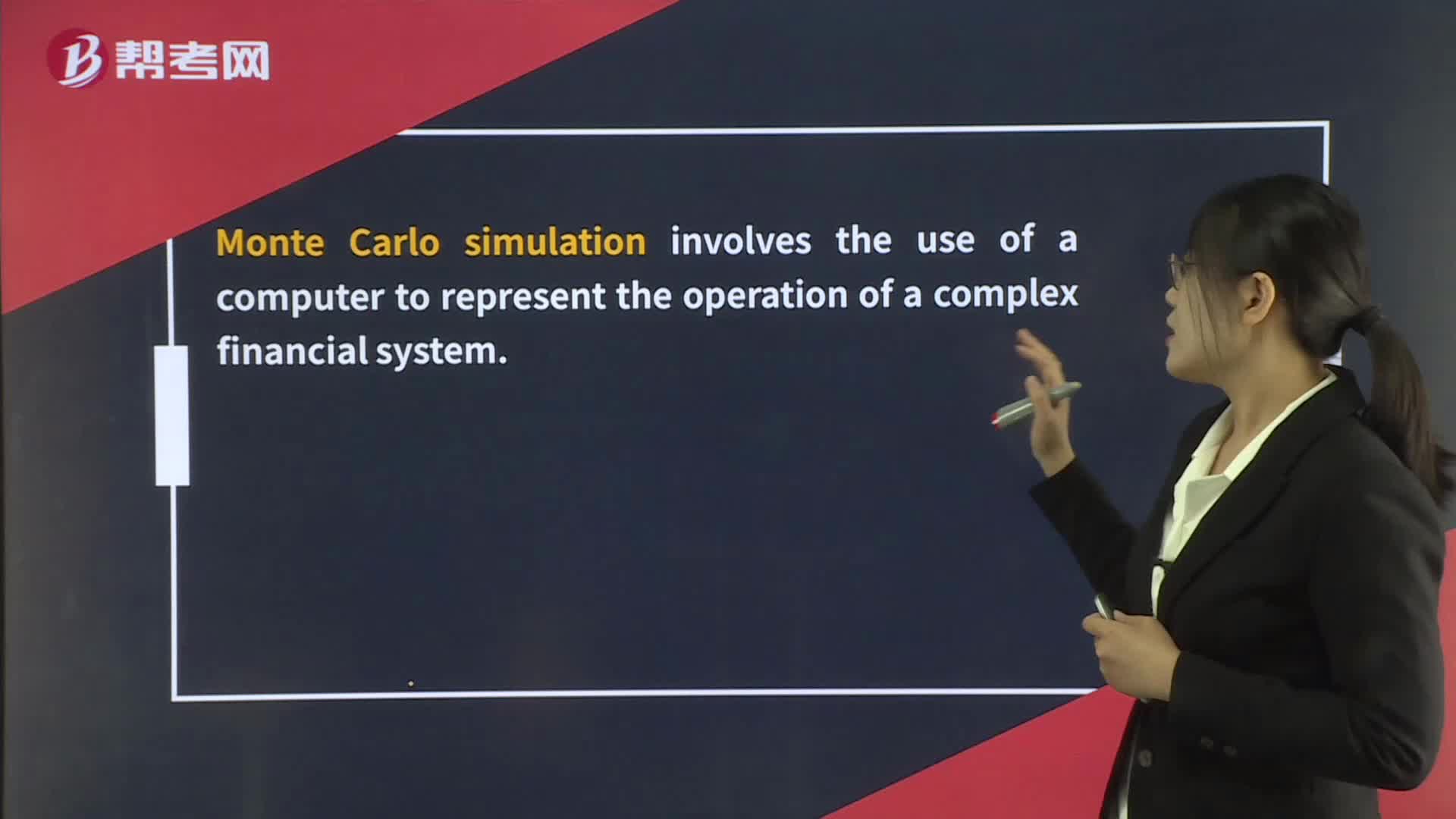

Monte Carlo simulation is a computational technique used to model and analyze complex systems or processes through the use of random variables and probability distributions. It involves generating a large number of random samples, simulating different scenarios, and calculating the outcomes based on the probabilities of various events occurring.

This simulation technique is widely used in finance, engineering, physics, and other fields where complex systems need to be analyzed. It is particularly useful for evaluating the potential risks and rewards of different investment strategies, assessing the reliability of complex systems, and optimizing decision-making under uncertainty.

The Monte Carlo simulation process involves the following steps:

1. Define the problem and the variables involved.

2. Determine the probability distribution of each variable.

3. Generate a large number of random samples for each variable based on its probability distribution.

4. Simulate the system or process using the random samples and calculate the outcomes.

5. Analyze the results and draw conclusions about the system or process being modeled.

Monte Carlo simulation can provide valuable insights into the behavior of complex systems and help decision-makers make more informed choices. However, it is important to note that the accuracy of the simulation results depends on the quality of the input data and the assumptions made about the system being modeled.

幫考網(wǎng)校

幫考網(wǎng)校