下載億題庫APP

聯(lián)系電話:400-660-1360

下載億題庫APP

聯(lián)系電話:400-660-1360

請謹(jǐn)慎保管和記憶你的密碼,以免泄露和丟失

請謹(jǐn)慎保管和記憶你的密碼,以免泄露和丟失

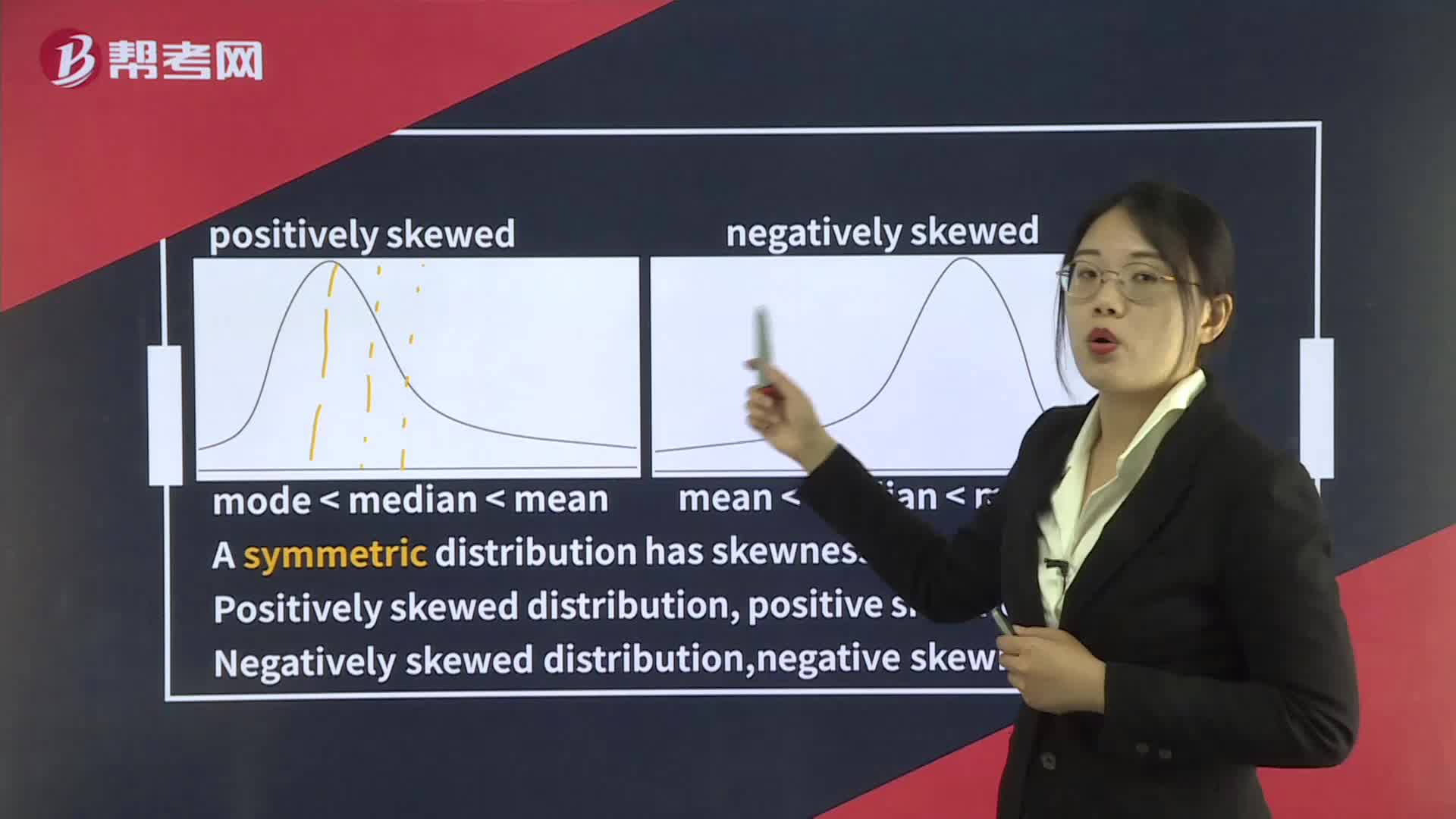

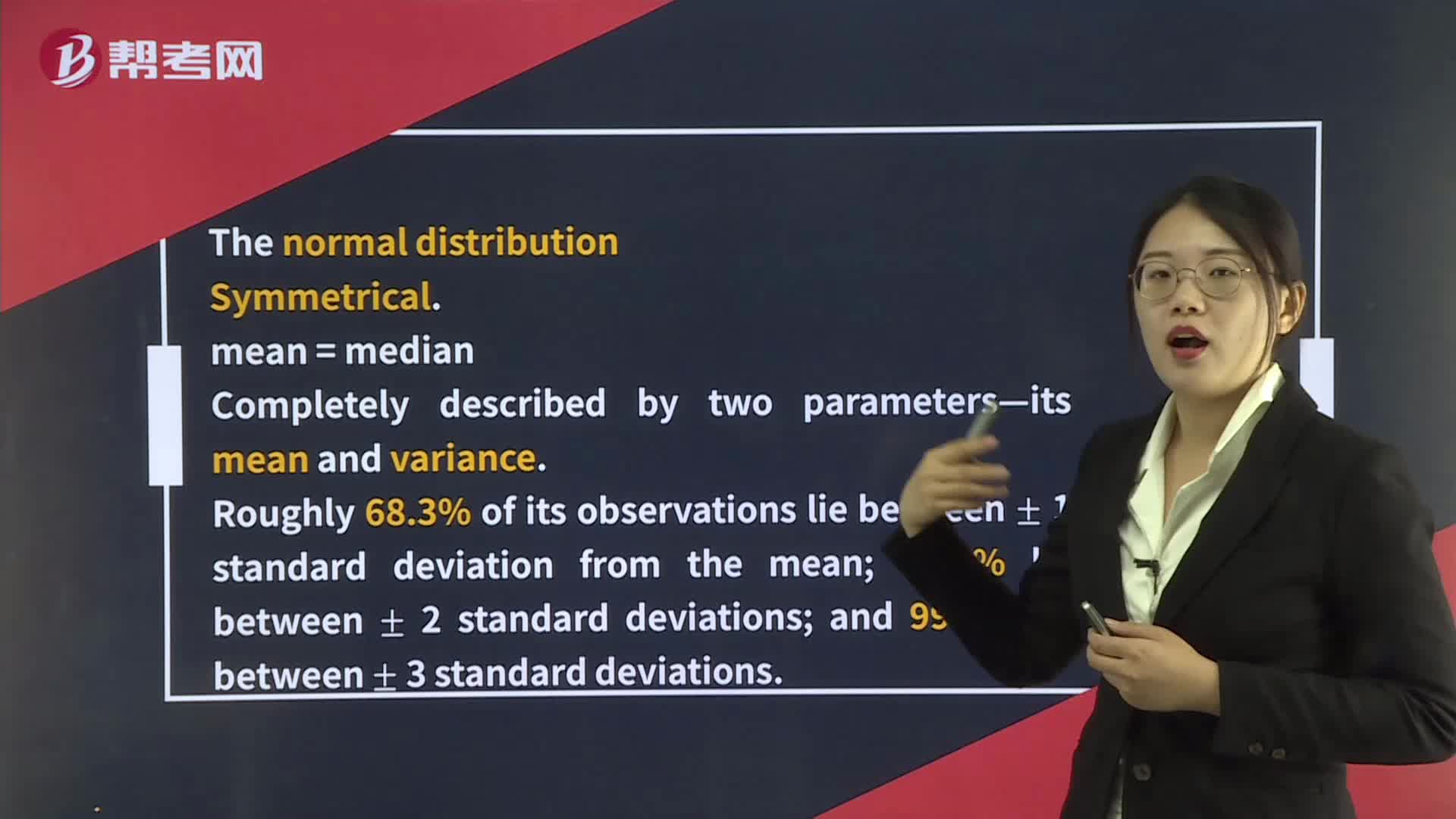

Skewness

微信截圖_1596769443898220200807111058057.png)

[Practice Problems] Two portfolios have unimodal return distributions. Portfolio 1 has a skewness of 0.77, and Portfolio 2 has a skewness of –1.11. Which of the following is correct?

A. For Portfolio 1, the median is less than the mean.

B. For Portfolio 1, the mode is greater than the mean.

C. For Portfolio 2, the mean is greater than the median.

[Solutions] A

Portfolio 1 is positively skewed, so the mean is greater than the median, which is greater than the mode.

199

199Skewness:which is greater than the mode.

644

644Symmetry, Skewness, Kurtosis:Symmetry,distribution,[Practice:A. For:C.[Practicereturns.C.

265

265What are the responsibilities of the members in reference to the CFA Institute?:Once accepted as a member:每年交述職報(bào)告和年費(fèi)but must not over promise the competency and future investment results.Case